A Model of Patient Spending and Movement Building

By NunoSempere, trammell @ 2021-11-08T18:00 (+93)

This project began during Nuño's 2020 summer research fellowship at FHI. Phil was the project mentor.

Motivation

The EA movement has tradeoffs to make about where to deploy its capital and labor. However, for now, these decisions seem like they are mostly made heuristically and intuitively.

To make those decisions more robust, we have set up a reasonably general model to try to capture the most important dynamics. We hope that the model is informative enough to influence decisions directly, and that it motivates more gathering and systematization of empirical data about variables that the model finds crucial (rate of expropriation, the shape of returns to movement building, etc.). We also hope that it inspires further modelling work.

Setup

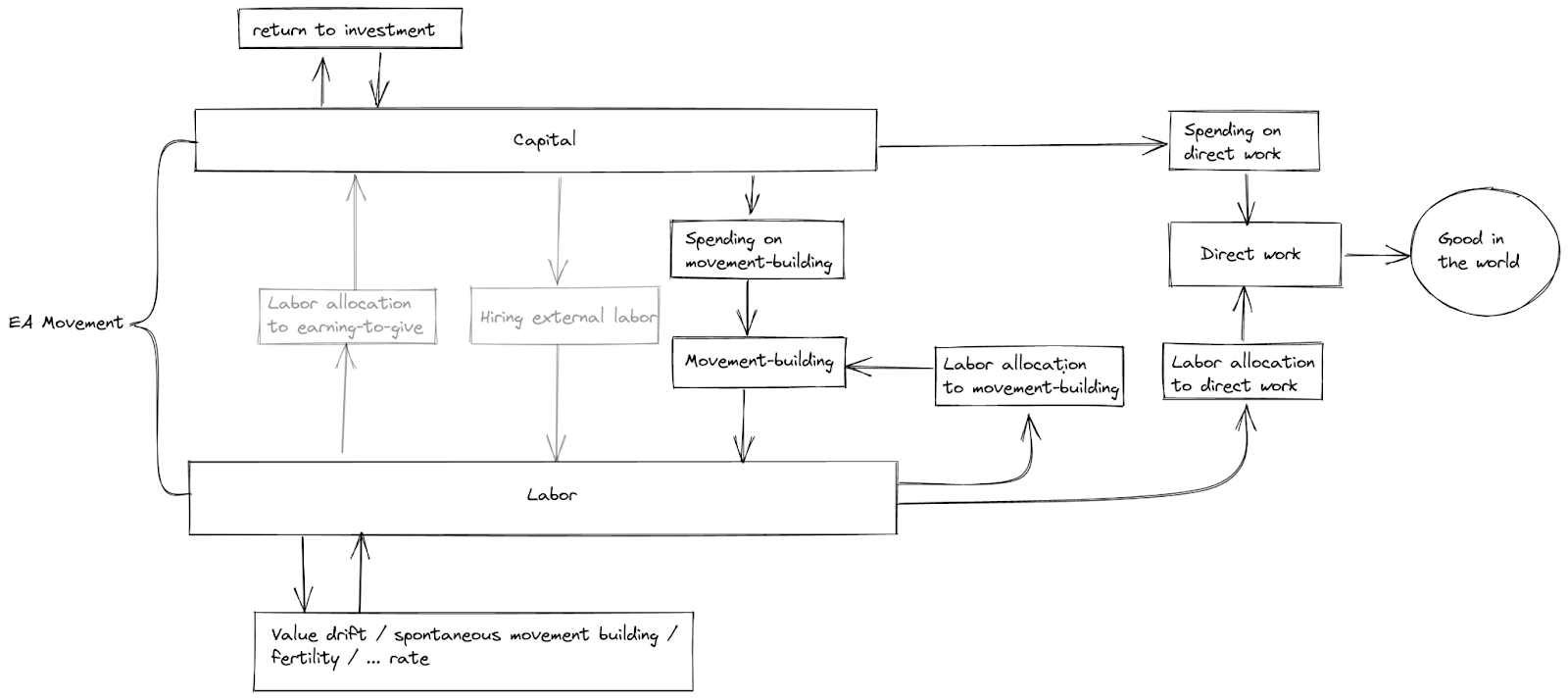

The model looks something like:

That is, the social movement has access to labor and capital.

In combination, they can be:

- Allocated to paid movement-building efforts, which return more labor

- Allocated to direct work, which returns goods in the world (malaria nets, etc.)

Alone, capital can be:

- Transformed into more capital with time

- Transformed into labor through hiring (only possible in one of the two models; this is why this step is greyed out in the diagram)

Alone, labor can be:

- Left alone to produce more labor, or decay, depending on the specifics of the model

- Allocated to earning to give, which returns more capital (only possible in one of the two models; this is why this step is grayed out in the diagram)

Note that the diagram only lays out the possible flows of labor and capital, but many parameters and functions determine how exactly that flow looks in practice. The paper defines these in more detail, but some which turn out to be important are:

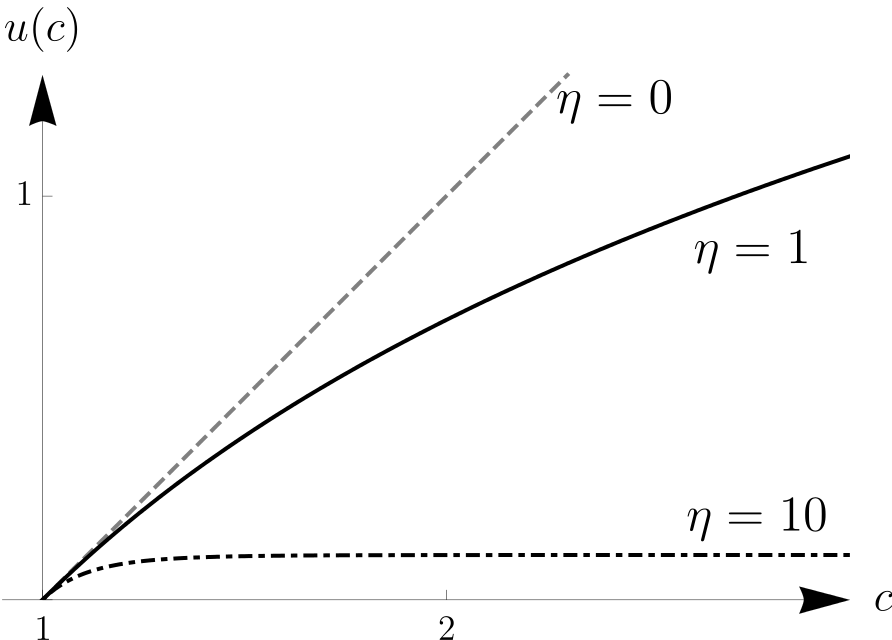

- Utility is isoelastic in "direct work", meaning that as the quantity of "direct work" (e.g., malaria nets delivered) increases, the utility function is assumed to have constant curvature, in a certain sense. For instance, as the number of malaria nets delivered increases, they get sent to places where the need for them is less great: this would imply a curvature that is less than linear. In our model, this curvature is represented by η. η = 1 defines a logarithmic utility function, η > 1 defines a function which exhibits sharper diminishing returns than the logarithm, and η < 1 defines a function that exhibits returns which diminish more slowly. (η = 0 defines linear utility.)

- Capital has a rate of return r

- δ is the “discount rate” (more technically, the time preference), i.e. the rate of intrinsically caring less about the future (pure time preference) we have—if any—plus the annual rate at which we collectively face risks of expropriation, value drift, existential catastrophe, etc.

- Labor, if left alone, depreciates (i.e., movement participants leave or die), at a rate d

- Labor productivity grows at a rate γ, to reflect the growing labor productivity seen in the economy as a whole

Using these functions and parameters, we set up a system in terms of rather general functions for the production of direct work and recruitment. We then solve it to arrive at the optimal solution, either across all points in time (if we allow for both earning to give and hiring) or only asymptotically (if we don't.)

If you are familiar with what the terms "isoelastic" and "constant elasticity of substitution" mean, you might want to just read the document.

Main results

If the social movement is "patient" (in that δ < r − γη), then under some reasonable assumptions about diminishing returns to movement building (see this comment), our model finds that total labor (i.e., total movement size) approaches a constant value. The fractions of labor that are allocated to direct work and movement building also approach a constant.

Spending on movement building and on direct work both grow exponentially, but at different rates (except under a knife-edge condition). Thus, eventually, close to all of the movement's spending will be directed to either movement building or direct work. This is because only one of the two can be the most efficient one at allowing capital to substitute for labor. That is, the movement eventually reaches either a Ponzi-esque state—where labor is much more scarce than capital and the best way to increase the absolute number of movement participants doing direct work is to use asymptotically all of its spending on movement-building—or a single-minded state where asymptotically all of its spending goes towards direct work.

We also make a tentative argument that the EA movement may not want to earn to give in the limit. The argument begins with the observation that, if both earning to give and hiring external labor are allowed, patient social movements generally want—in the long run—to hire external labor and have their participants do either direct work or movement building, but not earning to give. This suggests that, in the worlds where earning to give is feasible but hiring is not (at least for some tasks), patient movements will in the limit not want to engage in any earning to give.

Applications to Effective Altruism and Future Work

Though the results of the model are fairly straightforward, there are complications to consider when trying to apply them to real-world EA movement strategy. For instance, we are modelling movement participants as homogeneous. In reality, even though the model concludes that earning to give doesn't make sense in general in the limit, it might make sense for participants whose capacity to earn is far greater than their capacity to engage in direct work or movement-building. Also, note that any conclusion about the undesirability of earning to give is only asymptotic: we do not dispute that earning to give can be worthwhile early in a patient movement's timeline, if it does not yet possess enough capital.

In short, we think this model supports the intuitive idea that as capital accumulates, earning to give should eventually be phased out, though as noted we are uncertain about whether EA has reached that point already. Ultimately, our results depend on empirical parameters (value drift rate, the production function for movement building, salary rates, etc.), about which we are also uncertain. But uncertainty about parameter values can be reduced, and this should eventually allow our model to produce more concrete recommendations.

Another neglected complication is that our model doesn't address movement strategy when the movement can non-negligibly lower δ, e.g. by mitigating existential risks in the near term. It also fails to model the impact of doing research that makes future direct work and/or movement-building more efficient. We believe that extending the model to account for these complexities would be a valuable subject for future work.

Despite these caveats, the model has produced at least one important update for us. As the stock of EA capital has grown more quickly than the stock of EA labor, it has been widely claimed that earning to give is less valuable, relative to direct work, than it used to be. On a March 2020 episode of the 80,000 Hours podcast, Phil had argued that this claim was mistaken, on the grounds that the EA "capital to labor ratio" should simply be expected to fluctuate over time, suggesting that we had no reason to expect a long-run trend in either direction. Earning to give is thus still highly valuable, he argued, in light of the opportunity to invest for a time in which EA projects are again more capital-constrained. The results of our model suggest to us that this particular argument for earning to give was incorrect. It is at least plausible that, relative to direct work, earning to give has indeed grown less valuable, and—temporary fluctuations notwithstanding—will continue to do so.

MichaelDickens @ 2021-11-10T23:27 (+16)

Thanks for this! I think the setup is excellent, especially the diagram that makes it very clear what's going on. It seems basically comprehensive to me—not fully comprehensive, but it covers the most important stuff.

My approach when reading the full paper was:

- What are the interesting conclusions?

- What model assumptions produce those conclusions?

- Are any assumptions worth changing, and how might that change the conclusion?

The main conclusions, as I see it:

- Labor grows to a constant size, while capital keeps growing.

- Fraction of labor dedicated to earning-to-give approaches 0.

I like most of the assumptions, and I like that you can get interesting conclusions without knowing much about the parameter values.

I noticed three main things that I didn't see addressed (much) in the paper. From most to least important:

- Model assumes that labor experiences depreciation, while capital does not. But that's not true. Individuals who control capital might leave the movement; nonprofits that control capital might experience value drift. Prima facie, labor and capital should experience the same rate of depreciation[1]. The assumption of non-depreciating capital produced the results that (a) capital grows faster than movement size and (b) asymptotically 100% of laborers are hired from outside the movement. My intuition is that if you adjust this assumption, the optimal allocation will have both capital and labor asymptoting to a fixed size, and and , with asymptoting to 0. I'm less confident about this, but I'd guess that the optimal fraction of labor spent on earning-to-give would asymptotically equal the fraction of capital spent on recruiting, so that we're investing the same amount in both labor and capital.

This seems important because the assumption of depreciating capital is more realistic, and incorporating it would (maybe?) change both of the main conclusions.

If capital depreciates, but at a slower rate than labor, my intuition is that the optimal fraction of earning-to-give still approaches 0. If we model the movement as having "committed" members and "casual" members with different attrition rates, and with capital disproportionately coming from committed members, I'd guess you would find that (a) both labor and capital come almost exclusively from committed members in the long run, and (b) optimal earning-to-give fraction is a positive constant because committed labor and committed capital depreciate at the same rate.

Those adjusted conclusions are based on my intuitions. I'm not good enough at dynamic optimization to actually derive the solutions.

-

The paper briefly addresses this, but it's possible to recruit capital as well as labor by finding wealthy donors. (This is kind of the inverse of my first point.) Recruitment is zero-sum, so it can't be true in general that recruiting capital is easier than recruiting labor, but historically it looks like EAs have an easier time recruiting capital.

-

A patient movement cannot achieve market return indefinitely. Market return equals price change plus yield, and in the aggregate, investors do not re-invest their yield (I think?[2]). But patient investors always re-invest a positive portion of their yield, so their fraction of global wealth will increase over time. Eventually, this will decrease the rate of return on capital. This will take a long time (and might never happen in real life), but it matters when you're looking at asymptotic behavior.

A final note: I find it hard to read mathy papers that use a bunch of single-letter variables that are defined once in the middle of a paragraph, because I forget the definitions and then have trouble finding them again. It would be very helpful if the paper included a table of variable definitions.

[1] I would guess that, in practice, capital depreciates more slowly because capital is disproportionately controlled by the most committed members of the movement.

[2] Here is why I think this is true: For stocks, at least, the dividend yield comes from company earnings. In the long run, if the yield is constant, that means stock price growth equals earnings growth. If investors re-invest their dividends, which will push price growth above earnings growth, decreasing yield.

It's also possible that yield could decrease over time, but that gives the same conclusion—namely, that return on capital decreases.

Although I'm not sure that's how prices work, eg maybe stock prices are highly inelastic, so re-investing dividend yields doesn't cause them to go up significantly.

trammell @ 2021-11-11T02:02 (+3)

Thanks! A lot of good points here.

Re 1: if I'm understanding you right, this would just lower the interest rate from r to r - capital 'depreciation rate'. So it wouldn't change any of the qualitative conclusions, except that it would make it more plausible that the EA movement (or any particular movement) is, for modeling purposes, "impatient". But cool, that's an important point. And particularly relevant these days; my understanding is that a lot of Will's(/etc) excitement around finding megaprojects ASAP is driven by the sense that if we don't, some of the money will wander off.

Re 2: another good point. In this case I just think it would make the big qualitative conclusion hold even more strongly--no need to earn to give because money is even easier to come by, relative to labor, than the model suggests. But maybe it would be worth working through it after adding an explicit "wealth recruitment" function, to make sure there are no surprises.

Re 3: I agree, but I suspect--perhaps pessimistically--that the asymptotics of this model (if it's roughly accurate at all) bite a long time before EA wealth is a large enough fraction of global capital to push down the interest rate! Indeed, I don't think it's crazy to think they're already biting. Presumably the thing to do if you actually got to that point would be to start allocating more resources to R&D, to raise labor productivity and thus the return to capital. There are many ways I'd want to make the model more realistic before worrying about the constraints you run into when you start owning continents (a scenario for which there would presumably be plenty of time to prepare...!); but as noted, one of the extensions I'm hoping gets done before too long is to make (at least certain kinds of) R&D endogenous. So hopefully that would be at least somewhat relevant.

NunoSempere @ 2021-11-11T16:05 (+2)

Re: Labor grows to a constant size

Hey, in hindsight I realize that the paper + summarization don't make clear that this does depend on model assumptions/empirical points, sorry. I've edited the post to make this clearer (here is the previous version without the edits, in case it's of interest.)

tl;dr: This comes from model assumptions which seem reasonable, but empirical investigations + historical case studies, or alternatively sci-fi scenarios could flip the conclusion.

In particular, let , i.e. roughly , so each year you lose % of people, but you also do some movement building, for which you spend labor and capital.

Then for some functions f which determine movement building, this already implies that the movement has a maximum size. So for instance, if you have, then with infinite capital this reduces to

But then even if you allocate all labor to movement building (so that , or something), you'd have something like , and this eventually converges to the point where no matter where you start.

Now, above I've omitted some constants, and our function isn't quite the same, but that's essentially what's going on (see in equation 6 in page 4.) I.e., if you lose movement participants as a percentage but have a recruitment function that eventually has "brutal" diminishing returns (sub-linear diminishing returns to labor + throwing money at movement building doesn't solve it), you get a similar result (movement converges to a constant.)

But you could also imagine a scenario where the returns are less brutal—e.g., you're always able to recruit an additional participant by throwing money at the problem, or every movement builder can sort of eternally always recruit a person every year, etc. You could also imagine more sci-fi like scenario, where humanity is expanding exponentially (cubically) in space, and a social movement is a constant fraction of humanity.

More realistically, if instead looks like , which has diminishing returns but not brutally so, movement size can increase forever because you can always throw more money at the problem until

Note that if you have a less brutal recruitment function, this increases the appeal of movement building, not of earn to giving.

Also, I'm not sure whether "brutal" is the right way to be talking about this. "Brutal" is the term I use when I think about this but if I recall correctly the function we use is standard in the literature, and it seems plausible when you start to think about groups which reach a large size. But there is definitely an empirical question here about how movement results actually look like.

MichaelDickens @ 2021-11-14T17:53 (+4)

Hey, in hindsight I realize that the paper + summarization don't make clear that this does depend on model assumptions/empirical points

FWIW this was clear to me, I was using "conclusions" to mean "conclusions, given the model assumptions", not "conclusions, which the authors definitely think are true".

NunoSempere @ 2021-11-15T10:26 (+2)

Right, thanks, it seemed better to be too paranoid than to be too little.

Benjamin_Todd @ 2021-11-11T15:08 (+15)

Attempt to summarise the key points on Twitter:

NunoSempere @ 2021-11-11T17:41 (+4)

Hey Ben, see this comment, I think that this post originally did not make it clear that the constant size point does depend on empirical/reasonable model assumptions.

Daniel_Eth @ 2021-11-09T19:36 (+11)

This looks good! One possible modification that I think would enhance the model would be an arrow from "direct work" or "good in the world" to "movement building" – I'd imagine that the movement will be much more successful in attracting new members if we're seen as doing valuable things in the world.

trammell @ 2021-11-11T01:29 (+3)

Thanks! I agree that this might be another pretty important consideration, though I'd want to think a bit about how to model it in a way that feels relatively realistic and non-arbitrary.

E.g. maybe we should say people start out with a prior on the effectiveness of a movement at getting good things done, and instead of just being deterministically "recruited", they decide whether to contribute their labor and/or capital to a movement partly on the basis of their evaluation of its effectiveness, after updating on the basis of its track record.

Benjamin_Todd @ 2021-11-11T14:57 (+3)

A hacky solution is just to bear in mind that 'movement building' often doesn't look like explicit recruitment, but could include a lot of things that look a lot like object level work.

We can then consider two questions:

- What's the ideal fraction to invest in movement building?

- What are the highest-return movement building efforts? (where that might look like object-level work)

This would ignore the object level value projected by the movement building efforts, but that would be fine, unless they're of comparable value.

For most interventions, either the movement building effects or the object level value is going to dominate, so we can just treat them as one of the other.

Stefan_Schubert @ 2021-11-11T15:01 (+2)

I guess some sorts of earning to give may also attract new members. E.g. it wouldn't surprise me if Sam Bankman-Fried's work attracts some people to effective altruism.

NunoSempere @ 2021-11-11T00:56 (+2)

More off-the-cuff thought:

I can imagine that feedback loop (good in the world -> movement building) being important at the beginning. Arguably one of the reasons why the global health & development -> longtermism change of minds is so common is because longtermism has good arguments in principle but no big tangible wins to its name, so it's better able to convince those who pay attention to it because they're drawn to EA because of global health & development's big wins, rather than convince people directly.

But even in that case, if one wants longtermism to get a few big wins to increase its movement building appeal, it would surprise me if the way to do this was through more earning to give, rather than by spending down longtermism's big pot of money and using some of its labor for direct work.

Daniel_Eth @ 2021-11-11T10:19 (+1)

if one wants longtermism to get a few big wins to increase its movement building appeal, it would surprise me if the way to do this was through more earning to give, rather than by spending down longtermism's big pot of money and using some of its labor for direct work

I agree – I think the practical implication is more "this consideration updates us towards funding/allocating labor towards direct work over explicit movement building" and less "this consideration updates us towards E2G over direct work/movement building".

NunoSempere @ 2021-11-11T00:53 (+2)

This is a good point, and thanks for the comment.

If the arrow is from good in the world, this could increase the value of direct work and direct spending (and thus earning to give) relative to movement building. I can imagine setups where this might flip the conclusion, but I think that this would be fairly unlikely.

E.g., because of scope insensitivity, I don't think potential movement participants would be substantially more impressed by $2*N billions of GiveDirectly-equivalents of good per year vs just $N billions.

If the arrow is from direct work, this increases the value of direct work relative to everything else, and our conclusions almost certainly still hold.

I imagine that Phil might have some other thoughts to share.

Daniel_Eth @ 2021-11-11T10:15 (+3)

because of scope insensitivity, I don't think potential movement participants would be substantially more impressed by $2*N billions of GiveDirectly-equivalents of good per year vs just $N billions

Agree (though potential EAs may be more likely to be impressed with that stuff than most people), but I think qualitative things that we could accomplish would be impressive. For instance, if we funded a cure for malaria (or cancer, or ...) I think that would be more impressive than if we funded some people trying to cure those diseases but none of the people we funded succeeded. I also think that people are more likely to be attracted to AI safety if it seems like we're making real headway on the problem.

Patricio @ 2021-11-15T21:35 (+6)

I'm new to the movement so I have a couple of questions. Is it earning to give the only form of donations? Is there no one time big donors? and is Open Philanthropy included in there? and Givewell?

NunoSempere @ 2021-11-15T22:22 (+3)

Hey, good questions, thanks for cross-posting this from the EA Discord :)

OpenPhil is included in the model because the EA movement starts out with some capital. But convincing additional billionaires (or "earning to give" in the sense of "trying to become a billionaire to donate the billions to charity") is not modelled.

Also, the model does not (yet) include research, which is also part of what OpenPhil does.

One-time big donors could be modelled by increasing the initial capital, but this is kind of a kludge.

Also, once that small model exists, we can reason in ways like: The small model recommends doing direct work or movement building over earning to give, in the limit. Adding billionaires to the mix doesn't seem like it would change that property (unless "earning to give" includes "taking a shot at becoming a billionaire".)

Charles He @ 2021-11-15T22:17 (+3)

Is there no one time big donors? and is Open Philanthropy included in there? and Givewell?

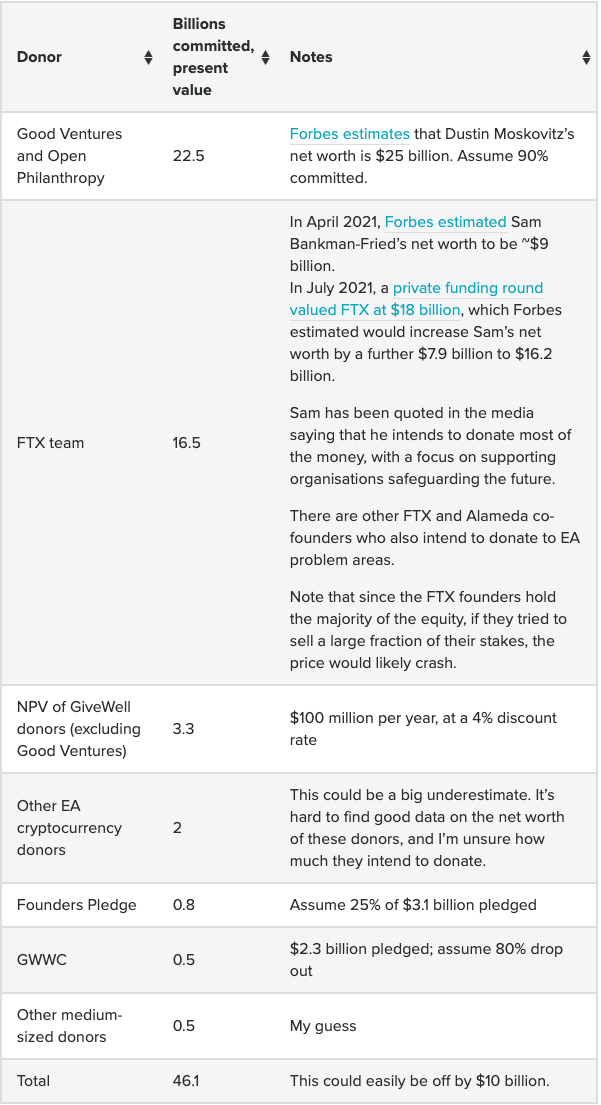

This 2021 post by Ben Todd gives a lot of detail about the financial resources of the EA movement. Here is a useful table:

It seems better to interpret GiveWell as a coordinator/distributor of money, not a source of money.

I'm uncertain what you mean when mentioning big one-time donors. Moskovitz and Bankman-Fried seem to want to donate the vast majority of their money, but for many reasons, it seems better to do this gradually.

Is it earning to give the only form of donations?

I'm not certain I understand what you mean, and you could be intending several different things.

Here's some verbose comments that might be helpful?

- It seems plausible to interpret all current sources of EA funding, including Sam Bankman-Fried, Dustin Moskovitz and Cari Tuna, as from earning to give.

- There is no major government source of direct funding if that is what you meant.

- More recently, there has been a push from EAs to coordinate or set policy from inside governments and institutions, they would redirect funding, resources or policy in some way. For example, they might change tax or trade policy, e.g. raising alcohol taxes. If you meant "in-kind" donations in some way, this is the only thing that comes to mind.

I'm not an expert and I'm not sure this comment was helpful.

Thank you very much for your interest and please feel free to clarify or ask anything else!

Patricio @ 2021-11-16T01:45 (+6)

Thank you for answering, it was helpful. So, with "other from of donations" I was referring to "one time donations". So both of your questions are about the same thing.

I understand that "earning to give" refers only to the donations that came from people who give a percentage of their income every month. At least it sounds like donations from people who are pledging on giving.

Either way if it is actually included or not, Nuno says that it's irrelevant.

Stefan_Schubert @ 2021-11-08T19:29 (+6)

That's interesting regarding earning to give.

In short, we think this model supports the intuitive idea that as capital accumulates, earning to give should eventually be phased out, though as noted we are uncertain about whether EA has reached that point already.

I guess that the claim that the fraction of people that earn to give should gradually be reduced is based on EAs having correct beliefs about the relative value of earning to give. If they originally underestimated the relative value of earning to give, and then correct that underestimate, it could be that they at least temporarily should increase the fraction of people that earn to give (I'm not claiming that, but just mention it as a possibility).

trammell @ 2021-11-08T22:18 (+3)

Good point, thanks!

MaxRa @ 2021-11-13T19:48 (+4)

One thought that came up to me is whether we should expect that EA stays a coherent movement over the longer term, or if EA ideas and values will be increasingly incorporated into mainstream culture over the coming decades. Then it might make less sense to draw a box around EA and model it as a separate thing from the rest of the world that contributes to the Good via direct work, right? E.g. I wonder how you would think about the current attempts to convince actors like the UN, or major governments, that thinking in much longer terms is great.

blonergan @ 2021-11-12T06:26 (+3)

Thanks for this interesting writeup and discussion!

I think EA movement building attracts people with different levels of commitment to EA. Doing direct work, at least given current salaries, might require most people to forgo 50-90% of their market income. This could mean people doing direct work will have a significant different lifestyle from people in their peer groups, particularly if the people doing direct work have children and do not have partners with high incomes.

People who find EA arguments compelling, but who are not willing to make the lifestyle sacrifice required to do direct work will find earning to give more appealing. Work often does not scale (down) well, so splitting one’s time between working for a market wage and doing direct work will tend not to be optimal.

This would change if direct work paid closer to market wages for different skillsets. More EAs could do direct work, and those who are more committed could donate greater shares of their income. But this could affect the culture within organizations (e.g. if colleagues had very different salaries or donated very different amounts), and lower salaries can serve a selection purpose for roles where the level of commitment to EA might affect job performance.

I’m not suggesting this needs to be in the model, but I think if direct work is an option only for highly committed EAs, it will affect the relative scarcity of labor and capital within the movement.

Charles He @ 2021-11-16T03:09 (+1)

Note that while Nuño says what is driving the labor results is the concave returns to recruitment, I think another stylized feature of the model is the depreciation of labor.

(I'm not fully sure this is correct and I didn't go through the model) but maybe to see this, notice that L and the model relies on d >0 (depreciation being strictly positive).

If d <= 0, the model seems to break, that is equation 8, has L negative or zero:

I didn’t do graduate macro theory (but I did dynamic structural IO), but I think it’s the canonically the opposite, typically capital (money) depreciates and labor deprecation isn’t standard (I'm happy to be corrected if wrong).

L represents the stock of EA labor, which in the model only rises through active recruitment and depreciates exogenously.

I'm not sure this EA labor depreciation is motivated empirically. It's plausible many EAs were not recruited actively but found the movement from online content or observing direct work. From other movements, it seems movements can grow geometrically for some time, without active, expensive recruitment.

Additionally, remember that like most models, the narrative works through long run effects in "equilibrium". It's less likely this applies to the ~12 year old EA movement, as opposed to national economies these models are typically used for.

So what?

If my writing above is somewhat correct, the point of this comment is that while models have value for rigor, there’s just a lot of assumptions and stylistic details baked in. It's important we are literate about this when communicating to non-experts and do not canonize or codify ideas inappropriately with models.

Ben Todd’s points in his recent talks e.g. EAG speech and the resources post, are important and correct. Movement money can grow faster than labor and EAs need to utilize greater resources effectively and alertly.

However, it's more plausible the reason the funding overhang exists is that we are in a long bull market and these capital markets have worked well for donors. Related to this, the crypto boom, combined with the focus, work and ability of Bankman-Fried and others have contributed precious resources.

This is probably more responsible for the funding overhang, as opposed to a concave return function to recruitment or depreciation of labor. It’s important to be aware of the effect of canonizing things with math.

Benjamin_Todd @ 2021-11-16T11:26 (+9)

We should keep reminding ourselves that FTX's value could easily fall by 90% in a big bear market.

NunoSempere @ 2021-11-16T08:45 (+7)

Hey, thanks for the comments. Your point about a bull market is welcome, and I think similar to the point that Phil made in the 80kh podcast. Some nitpicks:

- Nino -> Nuño

- When people say that "capital depreciates", they generally mean " capital investments", i.e., machinery, computers, etc.

- Note that labor depreciates at a rate d, in the sense that people move out of the movement because of value drift, but it also increases in value because of productivity improvements (see the exponentials in the model)

- I think that depreciation of labor is actually empirically motivated, e.g., by https://forum.effectivealtruism.org/posts/eRQe4kkkH2pPzqvam/more-empirical-data-on-value-drift

- But in models in which labor replicated itself (i.e., there was some "naturally arising movement-building"), we still didn't see that earning to give (in the sense of earning a salary) was favored in the limit either.

Charles He @ 2021-11-16T17:01 (+3)

I am sorry for the misspelling of your name. This is fixed.

This fault is mine, but it was not intentional, I think this was caused by autocorrect acting silently during writing.