Strategic wealth accumulation under transformative AI expectations

By arden, CalebMaresca @ 2025-02-21T13:16 (+14)

This is a linkpost to https://arxiv.org/abs/2502.11264

This is a linkpost with a summary of the key parts of Caleb’s new paper and its implications for EAs. You can read the original on arXiv here.

TL;DR

This paper analyzes how expectations of Transformative AI (TAI) affect current economic behavior by introducing a novel mechanism where automation redirects labor income from workers to those controlling AI systems, with the share of automated labor controlled by each household depending on their wealth at the time of invention. Using a modified neoclassical growth model calibrated to contemporary AI timeline forecasts, I find that even moderate assumptions about wealth-based allocation of AI labor generate substantial increases in pre-TAI interest rates. Under baseline scenarios with proportional wealth-based allocation, one-year interest rates rise to 10-16% compared to approximately 3% without strategic competition. The model reveals a notable divergence between interest rates and capital rental rates, as households accept lower productive returns in exchange for the strategic value of wealth accumulation. These findings suggest that evolving beliefs about TAI could create significant upward pressure on interest rates well before any technological breakthrough occurs, with important implications for actors in the EA community.

Interpretation. This post develops a model of household and firm decisions that may predict some aspects of economic behavior if beliefs about TAI timelines proliferate across the population. There are plenty of limitations and avenues for further research (explored in the conclusion), but the core findings remain powerful and possibly relevant to readers and philanthropic organizations.

Overview. Section 1 of this post is the introduction from the paper. Section 2 provides an explanation of the model developed in the paper and its intuitive interpretation, focusing on how expectations of a redistribution of labor based on capital imply different savings behavior than with expectations of a continuation of the status quo. Section 3 presents quantitative results, analyzing how different assumptions about TAI arrival probabilities and wealth-sensitivity parameters affect interest rates and capital accumulation. Section 4 explores implications for actors in the EA community. Section 5 concludes and suggests possible directions for future research. Sections 1, 3, and 5 of this post stay close to the paper, whereas sections 2 and 4 are substantially different.

If you’re looking to read something in between the TL;DR and the whole post, I’d recommend reading sections 1, 3, and 4. Using 265 wpm as an estimate, reading the TL;DR should take about 2 minutes, reading this middle version should take about 11 minutes, and reading the full post should take about 20 minutes.

Caleb wrote sections 1 and 5; Arden wrote sections 2, 3, and 4 drawing heavily from the paper.

1. Introduction

The accelerating pace of artificial intelligence (AI) development raises critical questions about its potential to reshape the global economy through two distinct yet interrelated mechanisms. First, AI systems capable of augmenting or replacing human researchers could dramatically accelerate scientific progress and economic growth, enabling parallel deployment of AI agents that rival human capabilities. Second, advanced AI—particularly artificial general intelligence (AGI)—could automate vast swaths of human labor, potentially concentrating economic benefits among capital owners while displacing workers. This looming possibility of automation may create novel incentives for strategic wealth accumulation today, as future control over AI labor could depend on wealth at the time of AI deployment. I term AI systems with these dual disruptive capacities Transformative AI (TAI), focusing on their specific economic implications.[1]

To analyze how forward-looking economic agents adjust their current decisions in anticipation of TAI’s uncertain arrival, this paper focuses specifically on the zero-sum nature of AI labor automation, distinct from AI’s productivity-enhancing effects. When AI automates a job - whether a truck driver, lawyer, or researcher - the wages previously earned by the human worker don’t vanish or automatically transform into broader economic gains. Instead, they flow to whoever controls the AI system performing that job. While AI will also generate new wealth through productivity gains (which this model captures through increased TFP growth), the reallocation of existing labor income creates immediate incentives for strategic capital accumulation.

To understand the full scope of TAI’s economic implications, let us examine each of these transformative mechanisms in detail.

The prospect of AI accelerating scientific advancement is particularly compelling given that the number of scientific researchers appears to be a crucial factor driving economic growth (Jones, 2005). If human-level AI is invented, many instances could be run in parallel, effectively multiplying the researcher population (Jones, 2022). Even without achieving human-level capabilities, AI systems could significantly enhance human researchers’ productivity. Moreover, AI’s ability to process and synthesize vast amounts of scientific literature could uncover connections that have eluded human scientists, who are necessarily limited in their capacity to absorb information (Agrawal et al., 2018).

Turning to TAI’s second major impact, its capacity for widespread automation raises important distributional concerns. Multiple leading AI developers explicitly pursue AGI systems that are “generally smarter than humans,”[2] which could render human labor economically obsolete across most domains. Unlike past technological disruptions that often created as many jobs as they eliminated, AGI could offer superior productivity across virtually all domains, potentially limiting the economic relevance of human labor. Unlike historical automation that created new roles, AGI might enable comprehensive substitution while concentrating returns: AI “laborers” would generate wealth, but ownership of these systems would likely remain with existing capital holders. This represents not merely job displacement but a structural shift in labor’s role—from human activity to AI-mediated capital service, benefiting those with more capital at the expense of others.

Crucially, even uncertain TAI prospects could reshape present-day economic behavior. Households anticipating TAI may alter consumption, savings, and investment patterns years before it materializes. These forward-looking adjustments imply that expectations alone—independent of realized technological change—could generate significant macroeconomic effects today. Understanding this anticipatory channel is essential for policymakers and economists navigating AI’s economic implications.

This work extends Chow et al. (2024) (post), who model TAI expectations as either explosive growth or existential catastrophe, finding that short-term TAI forecasts elevate long-term interest rates via Euler equation dynamics. While retaining their focus on growth scenarios, I introduce two critical and interrelated innovations: (1) explicit modeling of labor reallocation from human workers to AI systems disproportionately owned by wealthy households, and (2) strategic interactions in savings behavior as households compete for future control over AI labor.

The redistribution mechanism creates novel economic dynamics. Households’ post-TAI labor supply depends on accumulated capital, incentivizing strategic savings to secure larger shares of AI-mediated production. Savings thus become both wealth-building tools and claims on future AI labor—a zero-sum competition absent in standard growth models. This disrupts traditional capital-pricing relationships: interest rates must now compensate not just for capital’s rental rate but for the expected value of AI labor control rights.

This competitive dynamic creates a form of prisoner’s dilemma in savings behavior. While each household has an incentive to accumulate more wealth to secure a larger share of future AI labor, their collective actions to do so offset each other’s relative gains. Everyone saves more, yet no one achieves the relative wealth advantage they sought. This leaves all households worse off through reduced consumption, even though the underlying pressure to accumulate wealth remains. This strategic mechanism, distinct from standard productivity growth effects, helps explain why interest rates can remain substantially elevated even as increased capital accumulation drives down productive returns.

My findings reveal that expectations of TAI can substantially affect current economic conditions, even before any technological breakthrough occurs. Under baseline scenarios with proportional wealth-based allocation of AI labor, I find one-year interest rates rising to 10-16% compared to approximately 3% without strategic competition, highlighting how anticipation of TAI can incentivize aggressive wealth accumulation. The effects strengthen as wealth becomes more important in determining future AI labor allocation, though with diminishing returns. Notably, interest rates diverge markedly from capital rental rates during the transition period - while increased savings drive down the marginal product of capital, interest rates remain elevated due to competition for future AI labor control. This wedge between productive returns and interest rates represents a novel channel through which technological expectations can influence financial markets. The magnitude of these effects varies with the assumed probability distribution of TAI arrival, with more concentrated near-term probabilities generating sharper initial increases in interest rates.

This post proceeds as follows. Section 2 details the model setup and how it works, with a focus on the novel mechanism for AI labor allocation. Section 3 presents quantitative results, analyzing how different assumptions about TAI arrival probabilities and wealth-sensitivity parameters affect interest rates and capital accumulation. Section 4 explores implications for actors in the EA community. Section 5 concludes with policy implications and directions for future research.

2. Model

2.1 Allocation of AI labor

The key mechanism of this model is that in addition to assuming that the invention of TAI substantially increases economic growth, the paper also assumes that it transfers labor power from human workers to AI agents. In the struggle to determine who will control the labor income paid to AI agents, households with more capital at the time of TAI’s invention are assumed to have an advantage. Therefore, at the time when households become aware of TAI timelines, they begin to race for a greater share of aggregate capital in anticipation of the post-TAI advantage.

The share of AI labor allocated to each household at the time of TAI’s invention is given by this equation:

Where is the capital claims of the individual household at the time TAI is invented, is the aggregate capital at the time TAI is invented, and λ is a parameter that determines how sensitive the allocation of AI labor is to the wealth of the individual household.

When λ = 0, AI labor is distributed equally across the population regardless of wealth, implying no reallocation of labor. Conceptually, one can imagine that all human labor is automated, but each household is given an AI laborer (by the government or some other redistributing agency) exactly replacing their labor and leaving their economic situation unchanged. Equivalently, one can imagine that this corresponds to the outcome where TAI increases the growth rate but does not automate human labor. Therefore, this case is equivalent to Chow et al. (2024)[3] and will be useful for comparison. When λ > 0, wealthier individuals receive disproportionately more AI labor, with higher values of λ leading to a higher concentration of AI labor among the wealthy. λ = 1 corresponds to the case where AI labor is allocated proportionally to wealth, a household that is 10% richer when TAI is invented will be allocated 10% more AI labor. There is good reason to believe that λ may be significantly greater than one. Namely, race dynamics may cause differences at the top of the wealth distribution to be pivotal, whereas everyone else gets close to nothing. One can conceptually imagine this as that a large portion of households globally might not have nearly proportional access to investments if almost all their money mostly goes towards day-to-day necessities, barring them from partial ownership of data centers (or whatever it is). Investment in labs too, for example, is largely inaccessible today unless one is exposed through a venture fund, is an employee, or can buy difficult-to-find secondary market shares.

One can also consider λ < 0, whereby AI labor is distributed disproportionately toward poorer individuals. However, the paper does not focus on this case because it seems much more probable that wealth provides advantages in securing AI resources .

This allocation mechanism captures how control over automated labor becomes a zero-sum competition. Unlike traditional capital which can be produced to meet demand, the total supply of labor (human or AI) remains fixed in the model. When AI automates a task, it doesn’t create new labor - it redirects existing labor returns from human workers to AI owners. Any productivity enhancements from AI are captured separately through the increase in TFP growth rate from to . This modeling choice isolates the redistributive effects of automation from its productivity effects.

An alternative approach would be to model AI labor as a stock that can be accumulated through investment, similar to physical capital. This could better capture the possibility of expanding AI deployment over time. However, such an extension would significantly complicate the model’s dynamics by introducing a second type of capital with its own accumulation process and strategic implications. This promising extension is left to future research, with this paper focusing on the core mechanism of wealth-based allocation of a fixed labor supply.

2.2 Interest rate determination and the strategic wedge

In the standard model, the interest rate equals the marginal product of capital. However, in this model, capital ownership provides not only traditional returns but also a claim on future AI labor through the wealth-based allocation mechanism. This strategic component creates a wedge between interest rates and capital returns during the transition period between when households first become aware of TAI timelines and when TAI is invented: interest rates must compensate households not just for the standard opportunity cost of capital but also for giving up the strategic advantage that capital ownership provides in securing future AI labor.

Crucially, while this premium motivates each household to accumulate more capital than they would in a standard model, in equilibrium all households increase their savings similarly. Thus, no household actually realizes the full strategic premium - instead, they reach a Nash equilibrium where each household’s savings are optimal given others’ identical savings choices. The elevated interest rate reflects the intensity of this competitive dynamic: households must be compensated not just for postponing consumption, but also for the opportunity cost of not trying to “get ahead” in the strategic competition for future AI labor, even though in equilibrium all households end up with the same share.

This strategic competition creates a form of prisoner’s dilemma: all households would be better off if they could collectively agree to save at the rate implied purely by productivity growth expectations. However, the individual incentive to secure a larger share of future AI labor drives them to save more, pushing interest rates above capital rental rates even though the relative shares of AI labor remain unchanged in equilibrium. The size of this wedge increases with λ, as higher values make wealth differences more pivotal in determining post-TAI outcomes.

This mechanism explains why interest rates can remain elevated even as increased capital accumulation drives down the marginal product of capital. Even in periods well before TAI’s potential arrival, the anticipation of wealth-based allocation of AI labor influences household saving decisions and, consequently, equilibrium interest rates. This creates a wedge between both long-term interest rates and capital returns, and short-term interest rates and capital returns, though the magnitude and temporal pattern of these wedges may differ due to the different probability weights placed on near-term versus distant TAI arrival dates.

2.3 Other Assumptions

The economic growth rate prior to TAI () is assumed to be 1.8%, and after the invention of TAI () is assumed to be 30% as per Davidson (2021). This is of course much higher than the 2% historical average, though an increase of more than an order of magnitude is not without precedent. Prior to the industrial revolution, the world economy growth rate was near zero for most of human history (Roser et al., 2023). The model represents the economic growth rate as growth in the productivity of a given amount of capital and labor (TFP).

In the status quo, the wage bill is paid to human laborers and becomes income for the households who decide what to do with it. After TAI, the wage bill is paid to AI labor units owned by households.

Households are represented as expected lifetime utility maximizers, deciding in each period whether to consume a unit of that period’s income now, to invest that income in capital, or to invest that income in bonds. Household beliefs regarding the year in which TAI will be invented are treated as exogenous. While this assumption simplifies the analysis, it abstracts from plausible feedback mechanisms. For instance, the pace of AI development likely depends on endogenous factors such as private R&D investment and policy interventions, which could correlate with household expectations—especially under high values of λ, where wealthier agents anticipate disproportionate gains from automation. Nevertheless, the exogenous timeline assumption provides a tractable foundation for isolating the economic effects of belief-driven behavior.

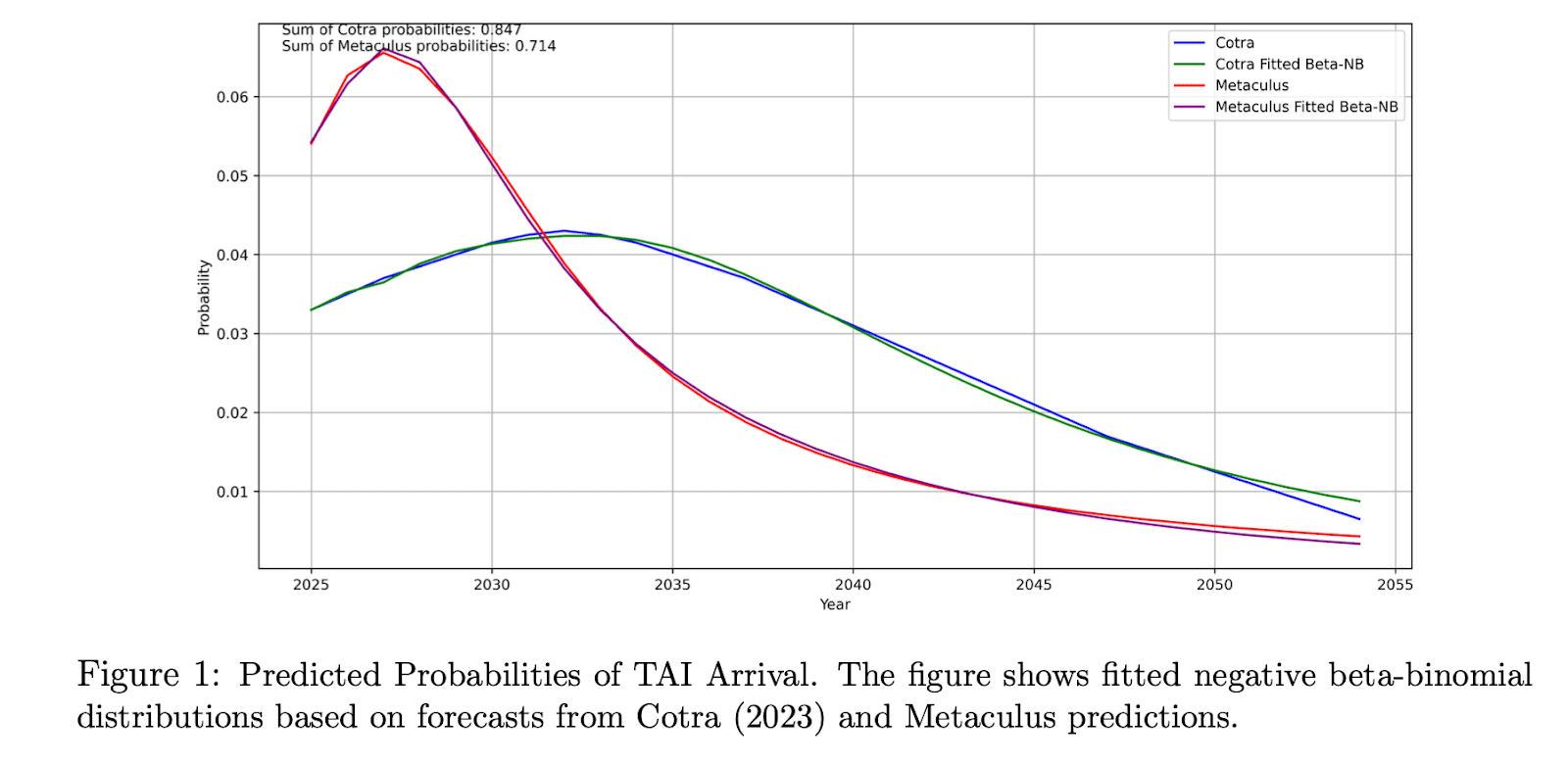

Households update timeline probabilities annually via Bayesian filtering. For the sake of tractability, current results focus on passive learning, wherein probability mass shifts from elapsed years to remaining possibilities as time progresses without TAI being invented. A possible extension could involve active learning, wherein households would update their posterior beliefs in accordance with the observed progress each year.

The yearly TAI probabilities are calibrated using two primary sources of AI timeline estimates: forecasts by Ajeya Cotra,[4] and aggregate predictions from Metaculus.[5] It’s important to note that they differ very considerably from the beliefs of the average household today, many of whom may not be attentive to changes in the AI landscape and who currently expect current economic conditions to persist. This paper hopes to consider what economic behavior would be expected if shorter timelines spread to the general population, so they seem good candidates for what those expectations might look like. The source probabilities and the fitted distributions are displayed here.

An interesting extension of the model could be to incorporate heterogeneous beliefs, where some fraction of households maintain status quo expectations while others anticipate transformative change, possibly with varying timeline distributions.

Using functional forms instead of directly applying the predictions from Cotra and Metaculus helps to smoothen the probabilities. In addition, it allows anyone to construct their own probability distributions and see how they affect the model.[6]

3. Results

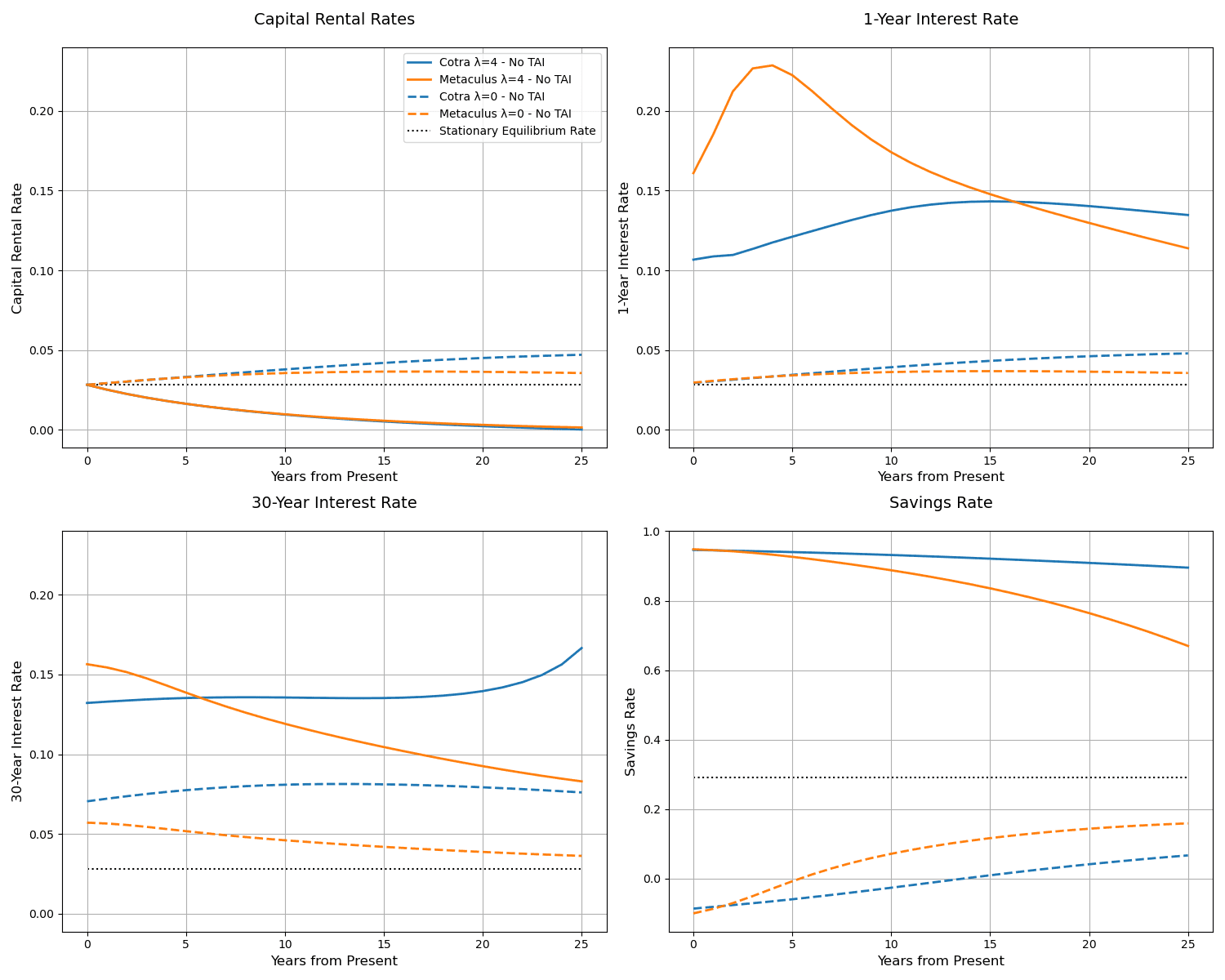

The model generates several key insights about how expectations of TAI affect interest rates, capital rental rates, and savings behavior. Capital rental rates are calculated using the marginal product of capital. Interest rates are calculated using Euler equations incorporating the strategic premium. The savings rate is calculated as (output − consumption)/output, representing the fraction of output not consumed.

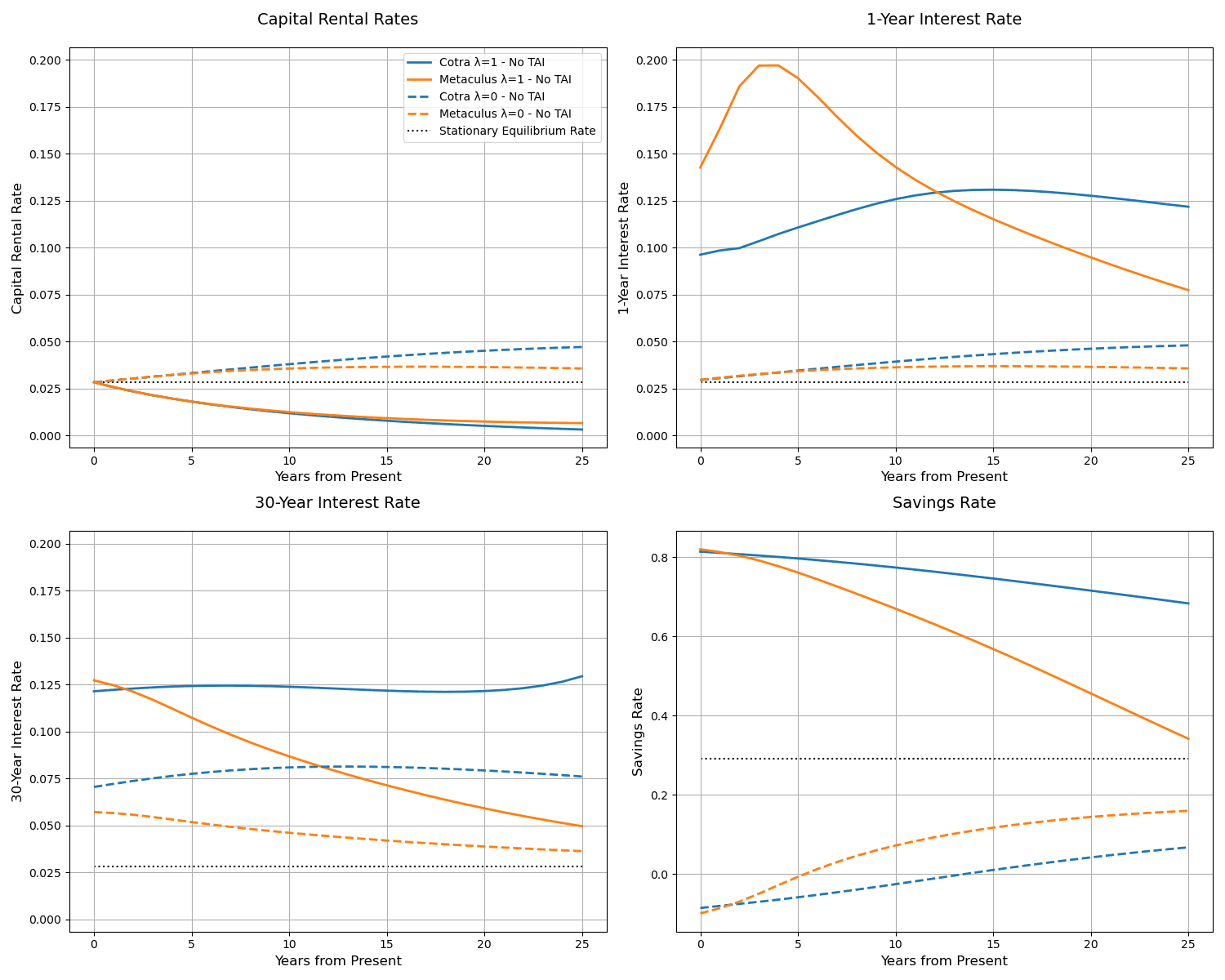

Figure 2 presents baseline results of λ = 1 under both Cotra and Metaculus probability distributions, while subsequent figures show comparative results under different values of λ, which governs the wealth-sensitivity of future AI labor allocation. All figures include the λ = 0 case (shown with dotted lines) as a benchmark that isolates pure growth expectations effects from strategic competition. The figures track pre-TAI rates—that is, rates in each year conditional on TAI not having occurred. If TAI does occur, interest rates quickly converge to a new equilibrium of approximately 35%, as implied by the standard stationary equilibrium in the neo-classical growth model given the assumed post-TAI growth rate of 30%.

Figure 2: Baseline Economic Outcomes (λ = 1). The figure shows predicted paths for capital rental rates, interest rates, and savings rates under proportional wealth-based AI labor allocation. Solid lines show outcomes with strategic competition (λ = 1), while dotted lines show the no- competition benchmark (λ = 0). Blue lines represent a Cotra probabilities world; orange lines represent a Metaculus probabilities world. The horizontal dotted line shows the stationary equilibrium rate without TAI expectations.

3.1 Baseline Case and Strategic Competition

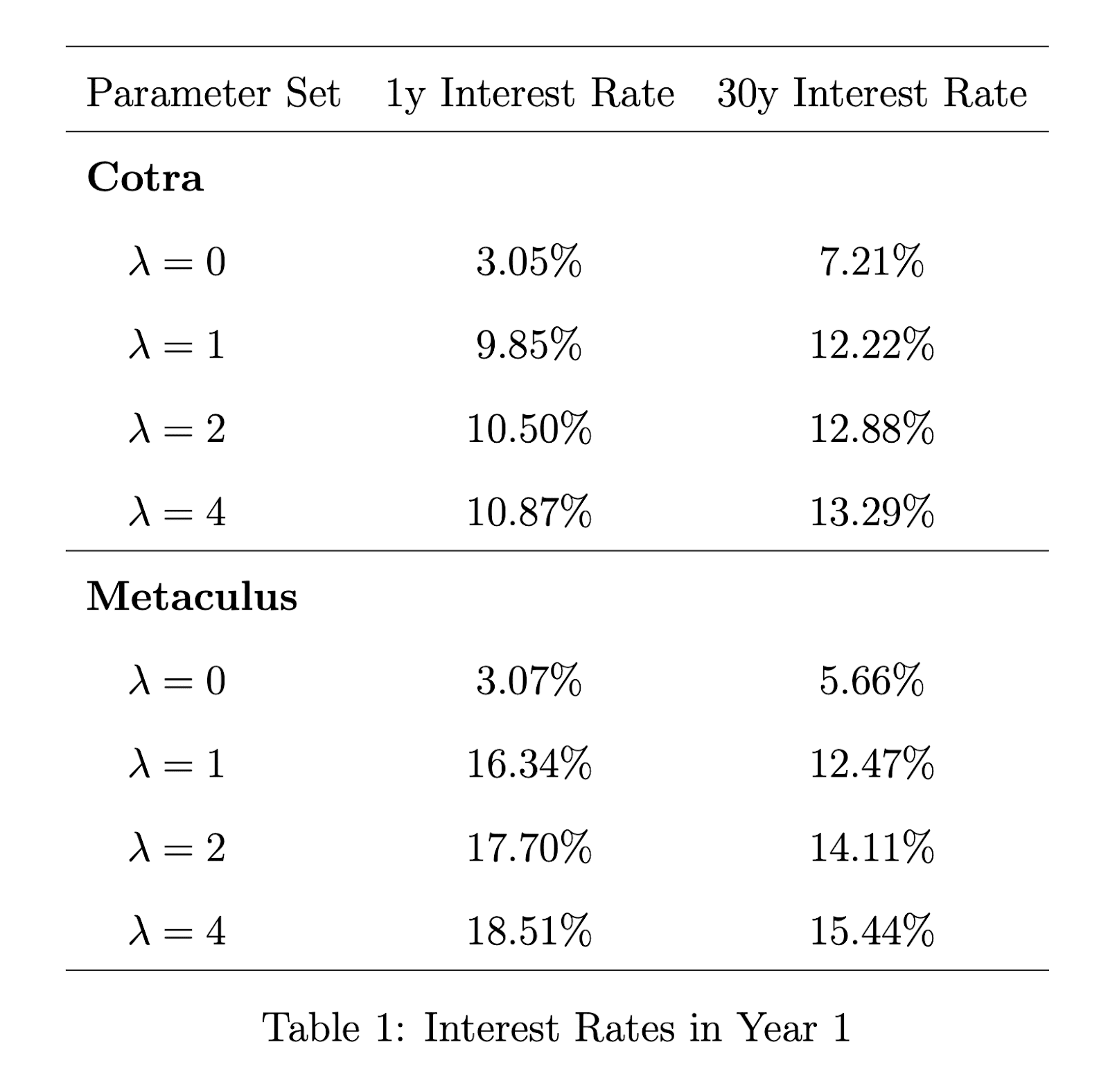

Baseline simulations reveal substantial effects of TAI expectations on interest rates. As shown in Table 1, with moderate assumptions about wealth-based allocation of AI labor (λ = 1), one-year interest rates begin at 9.85% under Cotra probabilities and 16.34% under Metaculus probabilities. This represents more than a tripling of rates compared to the no-competition scenario (λ = 0) where rates are 3.05% and 3.07% respectively. Thirty-year rates show similar elevation: under λ = 1, they rise to 12.22% and 12.47% for Cotra and Metaculus probabilities respectively, compared to 7.21% and 5.66% without strategic competition.

The time paths of these rates, shown in Figure 2, exhibit distinct patterns between the probability distributions. Under Metaculus probabilities, which assign higher likelihood to near-term TAI arrival, one-year rates spike dramatically in the first five years before declining, while Cotra probabilities produce a more gradual increase followed by a modest decline. This difference reflects the more concentrated near-term probability mass in the Metaculus distribution.

The λ = 0 case, shown in dotted lines across all figures, serves as an important theoretical benchmark, isolating the pure effect of growth expectations from strategic competition effects. While growth expectations alone generate modest increases in interest rates, the much larger increases seen with positive λ values highlight how strategic competition for AI labor control can substantially amplify these effects.

A notable feature of the model is the simultaneous presence of high savings rates and high interest rates during the transition period. As shown in Figure 2, savings rates begin at around 80%. Under Cotra probabilities they remain elevated for a long time while under Metaculus probabilities savings drop more rapidly. This contrasts with household behavior without strategic behavior (λ = 0), in which savings decline under standard parameterization, and are even negative for the first 5-12 years.[7][8] This shows the important impact of strategic savings: households save aggressively to secure future AI labor allocation despite high interest rates, creating a form of prisoner’s dilemma in saving behavior.

The savings rate predictions are admittedly extreme, suggesting that real-world frictions and behavioral constraints not captured in the model would likely moderate actual responses. However, the qualitative insight—that strategic competition for future AI labor can simultaneously drive up both savings and interest rates—remains relevant for understanding how TAI expectations might influence economic behavior. More realistic extensions to the model—such as incorporating heterogeneous beliefs, borrowing constraints, or gradual automation—could help generate more plausible savings behavior while preserving the core insight that strategic competition for future AI labor can simultaneously drive up both savings and interest rates.

3.2 Sensitivity to Wealth-Based Allocation

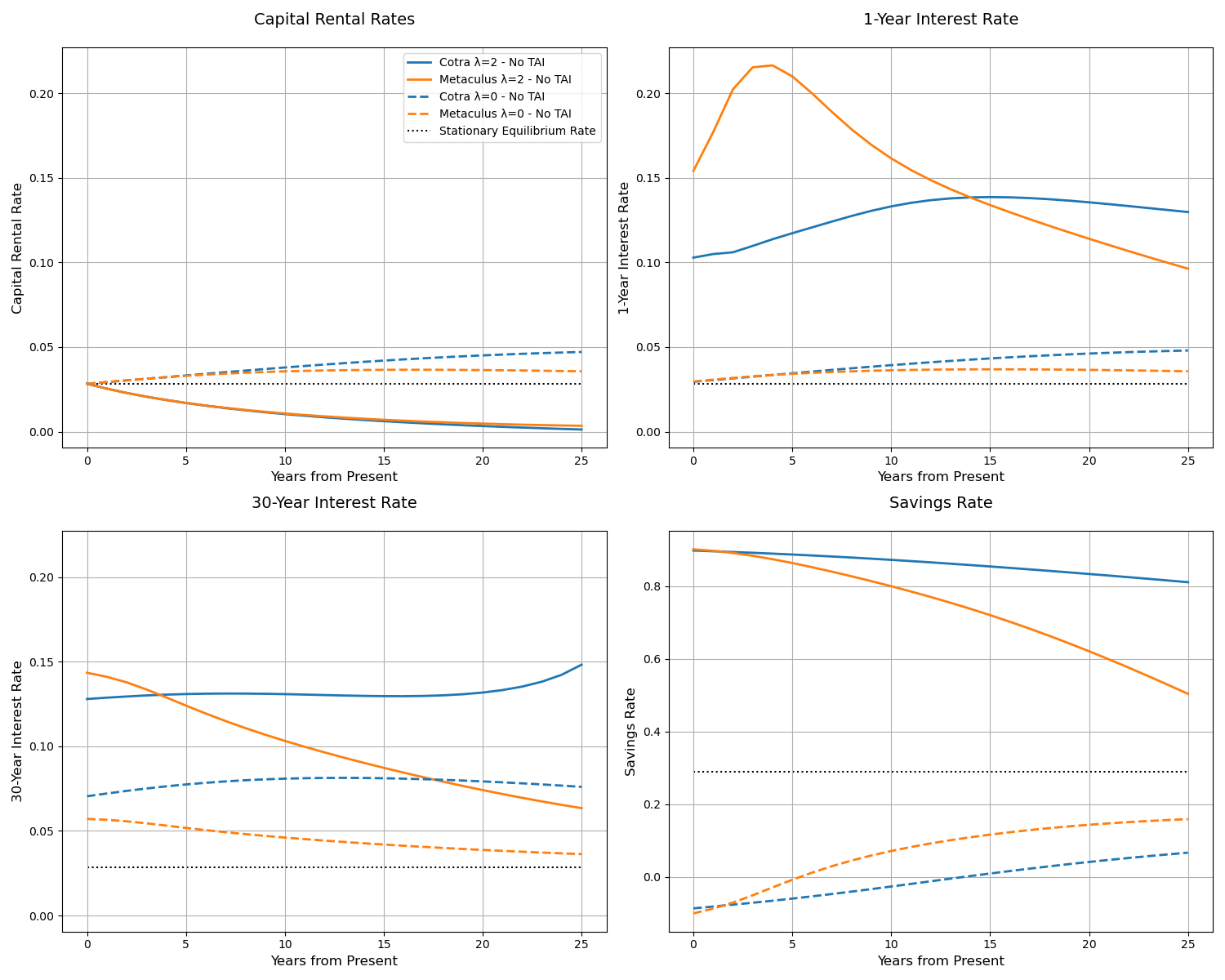

Figure 3: Economic Outcomes with Enhanced Strategic Competition (λ = 2).

Figure 4: Economic Outcomes with Strong Strategic Competition (λ = 4).

Figures 3 and 4 explore scenarios with stronger wealth sensitivity in AI labor allocation (λ = 2 and λ = 4 respectively). As λ increases, both short and long-term interest rates rise monotonically, reflecting intensified competition for future AI labor control. However, this effect exhibits diminishing returns: the increase in rates from λ = 0 to λ = 1 is substantially larger than subsequent increases.

For instance, under Metaculus probabilities, one-year rates increase by over 11 percentage points when moving from λ = 0 to λ = 1, but only by about 0.7 percentage points when moving from λ = 2 to λ = 4. This pattern suggests that while strategic competition for AI labor significantly affects interest rates, extreme sensitivity to wealth differences may not proportionally intensify these effects.

3.3 Capital Rental Rates

Capital rental rates show less dramatic variation across scenarios than interest rates and follow a generally declining pattern over time, reflecting capital accumulation. This divergence between interest rates and rental rates is particularly noteworthy: despite increasing savings driving down the marginal product of capital (as shown by falling rental rates), interest rates remain elevated due to strategic competition for future AI labor. This demonstrates how the prospect of TAI can break the traditional link between capital returns and interest rates, as households accept lower productive returns in exchange for the strategic value of wealth accumulation.

4. Implications for EAs

Notably, all scenarios with positive λ produce interest rates substantially higher than the no-competition benchmark. Even modest assumptions about wealth-based allocation of AI labor lead to dramatic increases in rates. This finding extends Chow et al. (2024), whose representative agent model is equivalent to this model with λ = 0. Importantly, λ is plausibly greater than or equal to one if wealthier households can spend more to run proportionally more AI agents or if there exist barriers in the form of something like minimum investment amounts or race dynamics at the top of the wealth distribution that become very important. In these cases, TAI expectations could cause interest rates to rise far higher than the rates predicted by previous models, as shown in Table 1. These findings have important implications, as they suggest that evolving beliefs about TAI could create strong upward pressure on interest rates well before any technological breakthrough occurs.

Most importantly, these results imply that it might be important for EA charities concerned about AI safety to hedge against high interest rate environments in the event that short timelines are more widely adopted and seem more likely. Short timeline worlds are plausibly the most dangerous worlds from an AI safety perspective and would deserve extra resources devoted towards AI safety research in the time before TAI is invented. High interest rates hedges for the next 3 or 10 years would effectively pull resources from worlds where long timelines are more likely into worlds where short timelines are more likely, where these resources would be much more impactful. I will not speculate here on the best ways to put on this hedge, but its possible importance should not be understated. If we want to spend a ton of money on AI safety in the next 5 years conditional on short timelines seeming more right and being taken more seriously (extreme cases being the introduction of something like an AGI Manhattan Project), we should be placing bets that pay a ton of money on that same conditional.

On the policy side, these results suggest that something like a UBI somehow tied to AI usage might be particularly useful in that such a policy would minimize λ. This would yield benefits not only in the post-TAI world when much of the population might not be able to find employment, but also once the population becomes more broadly aware of TAI timelines because it could avoid much of the zero-sum saving dynamic.

For readers more generally, these results imply that before TAI timelines become widely known, it may be reasonable to cut down on consumption and focus on building up savings and investments.[9] This may not be true if one has particularly pessimistic expectations about AI doom, or if one believes that TAI would bring nearly instant overwhelming abundance (very much higher than 30% yearly economic growth), but seems prescient if one thinks the relevant assumptions taken in this model are plausible. As alluded to in Chow, et al. (2024), there is probably also alpha in certain interest rate bets if one believes in short timelines, but these probably become substantially harder without access to the kinds of illiquid derivatives where these beliefs could probably most directly be expressed.

5. Conclusion

This paper develops a theoretical framework for analyzing how expectations of Transformative AI (TAI) could influence current economic behavior, with particular attention to the effect of wealth-based allocation of automated labor. The model reveals that anticipation of TAI can significantly affect present-day interest rates and capital accumulation patterns through two distinct channels: expectations of higher future growth and strategic competition for future AI labor control.

The model reveals an important game-theoretic aspect of this strategic competition. While individual households are incentivized to accumulate wealth to secure larger shares of future AI labor, in equilibrium all households increase savings similarly. This creates a prisoner’s dilemma where competitive wealth accumulation drives up interest rates without changing relative shares of future AI labor. This finding suggests that expectations of TAI could generate substantial financial market effects even when the strategic benefits of wealth accumulation are ultimately neutralized by equilibrium behavior.

This strategic dynamic manifests not only in elevated interest rates but also in extremely high savings rates. While such extreme savings predictions likely overstate real-world behavioral responses, they highlight how strategic competition fundamentally amplifies saving incentives.

A key finding is that the strength of wealth-based allocation in determining future AI labor shares (parameterized by λ) monotonically increases both short and long-term interest rates, though with diminishing returns. This suggests that while strategic competition for AI labor significantly affects financial markets, extreme sensitivity to wealth differences may not proportionally intensify these effects. Moreover, the model reveals a notable divergence between interest rates and capital rental rates, as households accept lower productive returns in exchange for the strategic value of wealth accumulation.

Several promising directions for future research emerge from this analysis. First, relaxing the assumption of homogeneous initial wealth could provide insights into how TAI expectations might affect wealth inequality dynamics. Second, incorporating heterogeneous beliefs about TAI arrival probabilities would better reflect real-world variation in technological expectations across different economic agents. Third, extending the model to include active belief updating based on observed technological progress could capture how evolving information about AI development influences economic behavior.

Additional extensions could explore the role of takeoff speed in shaping economic responses to TAI expectations. While the current model assumes an immediate transition to higher productivity growth, a more gradual takeoff might generate different patterns of anticipatory behavior. TAI could even result in superexponential growth (Aghion et al. 2017, Trammell and Korinek 2023), which could boost interest rates even further and have additional effects on long-term bonds. Furthermore, building on Chow et al.’s findings, incorporating TFP shocks could illuminate how increased growth volatility might counteract or amplify the interest rate effects identified in this paper.

In conclusion, this analysis demonstrates that expectations of TAI can substantially influence current economic behavior through both growth expectations and strategic wealth accumulation motives. As AI technology continues to advance, understanding these anticipatory channels becomes increasingly important for economic policy and planning. Future research extending this framework along the directions outlined above will be crucial for developing a more complete understanding of how technological expectations shape economic outcomes.

Thanks to Philip Trammell, Basil Halperin, and J. Zachary Mazlish for excellent comments and suggestions.

- ^

This operationalizes Gruetzemacher and Whittlestone (2022)’s definition of Transformative AI as “Any AI technology or application with potential to lead to practically irreversible change that is broad enough to impact most important aspects of life and society. One key indicator of this level of transformative change would be a pervasive increase in economic productivity.”

- ^

- ^

Ignoring the possibility of existential catastrophe.

- ^

I selected yearly probabilities to roughly align with https://www.alignmentforum.org/posts/AfH2oPHCApdKicM4m/two-year-update-on-my-personal-ai-timelines and https://www. alignmentforum.org/posts/K2D45BNxnZjdpSX2j/ai-timelines

- ^

- ^

An interesting further project could be to build a tool where anyone can input their beliefs in terms of the parameters of the distribution (a discrete distribution encapsulating your uncertainty over how many 'breakthroughs' are necessary for TAI, and alpha and beta - which determine the beta distribution from which the monthly breakthrough probabilities are drawn from) and receive the yearly TAI probability distribution, the 1-year, and the 30-year interest rate plots given the distribution.

- ^

Negative savings indicate that households are consuming more than current output by depleting their capital stock, reflecting their desire to front-load consumption in anticipation of higher future productivity.

- ^

It is possible that savings could rise even with λ = 0 under smaller coefficients of relative risk aversion.

- ^

Nothing in this post is financial advice.

Matthew_Barnett @ 2025-02-21T22:25 (+8)

While AI will also generate new wealth through productivity gains (which this model captures through increased TFP growth), the reallocation of existing labor income creates immediate incentives for strategic capital accumulation.

I'm worried that some of the most important results of this model hinge critically on the fact that you're modeling new wealth via AI's impact on TFP, rather than modeling AI as a technology that increases the labor supply or the capital stock (in addition to increasing TFP through direct R&D).

In particular, I find your claim that AI creates a "prisoner's dilemma" scenario—where households aggressively save in order to secure a larger relative share of future wealth but, in doing so, reduce overall consumption—potentially misleading. In my view, household savings will likely play a crucial role in funding the investments necessary to build AI infrastructure, such as data centers. These investments accelerate the development of transformative AI, which in turn hastens the economic benefits of AI.

From this perspective, high savings rates are not collectively irrational or self-defeating in the way suggested by a "prisoner's dilemma" framing. On the contrary, increased savings directly affects how soon transformative AI arrives, enabling higher consumption earlier in time, which increases time-discounted social welfare.

CalebMaresca @ 2025-02-22T15:05 (+4)

Hi Matthew,

Thank you for your comment. I think this is a reasonable criticism! There is definitely an endogenous link between investment and AI timelines that this model misses. I think that this might be hard to model in a realistic way, but I encourage people to try!

On the other hand, I think the strategic motivation is important as well. For example, here is Satya Nadella on the Dwarkesh Podcast:

And by the way, one of the things is that there will be overbuild. To your point about what happened in the dotcom era, the memo has gone out that, hey, you know, you need more energy, and you need more compute. Thank God for it. So, everybody's going to race.

In reality, both mechanisms are probably in play. My paper is intended to focus on the race mechanism.

Two more notes: higher savings imply lower consumption in the short term. However, even if TAI isn't invented, consumption will rise higher than in the stationary equilibrium purely from capital accumulation.

Lastly, the main thrust of the paper is on the implications for interest rates, I do not intend to make strong claims about social welfare.

SummaryBot @ 2025-02-21T19:10 (+1)

Executive summary: Expectations of transformative AI (TAI) significantly impact present-day economic behavior by driving strategic wealth accumulation, increasing interest rates, and creating a competitive savings dynamic as households anticipate future control over AI labor.

Key points:

- Dual Economic Impact of TAI – TAI could accelerate scientific progress and automate vast sectors of human labor, concentrating wealth among capital holders while displacing workers.

- Wealth-Based AI Labor Allocation – Ownership of AI systems determines who benefits from automated labor, creating incentives for strategic savings as households compete for future AI labor control.

- Prisoner’s Dilemma in Savings – Households engage in aggressive wealth accumulation, driving up interest rates (potentially to 10-16%) without gaining a relative advantage, reducing overall consumption.

- Financial Market Implications – The model predicts a divergence between capital rental rates and interest rates due to competition for AI labor control, with higher wealth sensitivity (λ) amplifying this effect.

- Implications for EA and Policy – EA actors should consider hedging against high interest rate environments if short AI timelines become widely accepted, while policymakers could mitigate wealth concentration through AI-tied UBI.

- Future Research Directions – Suggested extensions include modeling heterogeneous beliefs, gradual AI takeoff speeds, and endogenous feedback mechanisms to refine economic predictions.

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.