What you really mean when you claim to support “UBI for job automation”

By Deric Cheng @ 2024-05-14T08:26 (+22)

Author’s Note: Crossposted from LessWrong. Though I’m currently a governance researcher at Convergence Analysis, this post is unaffiliated with Convergence. The opinions expressed are solely my own.

You’ve seen it a dozen times at this point. You’re probably broadly aligned philosophically, but haven’t thought terribly deeply about the details. You generally support Andrew Yang’s $12k / year “Freedom Dividend” as “moving in the right direction”, even if it’s economically flawed.

The argument goes roughly like this: “All of our jobs are about to be automated away with AI technology and robotics! We’ll end up soon in a post-work society with massive unemployment unless we can find a way to distribute the benefits of AI automation fairly. We need a universal basic income to protect humans.”

To recap - universal basic income is a proposal to give every individual in a society a sum of money on a monthly or annual basis, to provide a “universal safety-net” for those who are unemployed or enable greater financial flexibility. A very common proposal for the US is on the order of $1k a month, or $12k a year[1].

Personally, I’m fairly aligned with the direction of this argument. But it strikes me as painfully simplistic. Our social welfare systems have been incrementally built over decades, targeting measurable improvements for vulnerable demographics. Effective taxation and redistribution is dependent on thousands of economic factors, with winners and losers for every decision.

So - I decided to explore. What would an actual implementation of “UBI in the face of increasing job automation” look like? As a casual proponent, what specific policies do you actually support to achieve your socioeconomic ideals?

A couple big takeaways from this research:

- Part 1: If your goal is a universal safety net, you probably don’t actually want UBI. You want some form of a targeted negative income tax (NIT) that also provides direct payments. In practice, you might only want minor (US) policy tweaks to the Earned Income Tax Credit (EITC).

- Part 2: If your goal is to transfer the wealth generated by automation, you probably actually want global tax reform to better enforce corporate income taxes. You might also support some form of a progressive income tax on the largest multinational corporations.

Let me share a hot take. After doing this research, I think that if you support UBI (as popularly structured as a $X,000 monthly benefit for every citizen), it’s not because it’s an economically sound proposal. It’s because it aligns with your ideological stance, is easy to reason about, and trendy in the public discourse.

I’ll explore Part 1 in the post below. Let’s dive in!

Quick Assumptions

- I’m going to focus specifically on US policy here. Why? Well, in part because it was plenty complicated for me to evaluate just the US.

- More concretely - revising a single nation’s social welfare system is realistic and has precedents for implementation. Global wealth redistribution via governance is well outside the Overton window and I don’t see a clear path for the political support to arise yet.

Most of the big “AI overlord” corporations we’re worried about are based in the US. Presumably, if a global “UBI for job automation” were to be mandated, it would have to be aligned with US policy[2].

- I’m going to focus on practical government policy, rather than proposed charitable & voluntary donations by individual AI corporations.

- Sure, it’d be great if the people at the top of the capitalist food chain eventually decide to reject capitalism for the good of human society. I’m not counting on it myself.

- Everything is highly, HIGHLY simplified. This is a concise opinion piece, not a comprehensive report. I’d love to discuss relevant details in the comments.

It’s easy to want Universal Basic Income. It’s not easy to pay for it.

Let’s jump straight to the obvious problem - such a program is absurdly expensive. Chugging the basic numbers: $12k per person, with roughly 330 million Americans, is $3.96 trillion per year. The federal budget is currently $6.1 trillion per year. So a UBI would immediately increase the entire federal budget by ~40%.

Of course, there are tons of ways to reduce this overhead[3]. In particular, UBI is designed to simplify and replace income welfare programs, such as food stamps or unemployment benefits. These add up to roughly $450 billion. In particularly extreme arguments[4], it replaces all of Medicare, Medicaid, and Social Security, which add up to $2.75 trillion[5]. Altogether, every social welfare program combined is still much less than the proposed cost of UBI.

Replacing social welfare with UBI 1:1 is regressive

The problem with paying for UBI by reducing social welfare is that in essence, such a redistribution is regressive (in the sense of a regressive tax).

What that means is: every dollar you move from unemployment benefits to UBI is money moving from unemployed people to more-employed people. Redistributing money from Medicaid is moving money from low-income to higher-income earners. And so on[6]. Paying for UBI primarily by replacing social programs would actually have the net opposite effect of what you wanted from UBI, which is more security for the disadvantaged[7].

So to pay for UBI, we probably need to raise taxes[8]. Significantly.

Let’s assume, for right now[9], a majority of that will come from individual income taxes and payroll (Social Security / Medicare) taxes, which make up 86% of the US’s $4.4 trillion in revenue. At the very least, we’d need to restructure our entire individual income tax system to at least somewhat accommodate for that ~40% budget increase.

For most people, UBI is just a tax credit (and maybe higher taxes)

This brings us to the next point, which seems obvious when you think about it. Any individual paying above $12k in taxes wouldn’t actually receive payments from the government - they’d receive a tax credit equivalent to $12k a year. As per the “leaky bucket” theory, I think almost everyone is against the idea of paying higher taxes to the IRS, only to have the IRS mail them back that same money via a UBI check once a month.

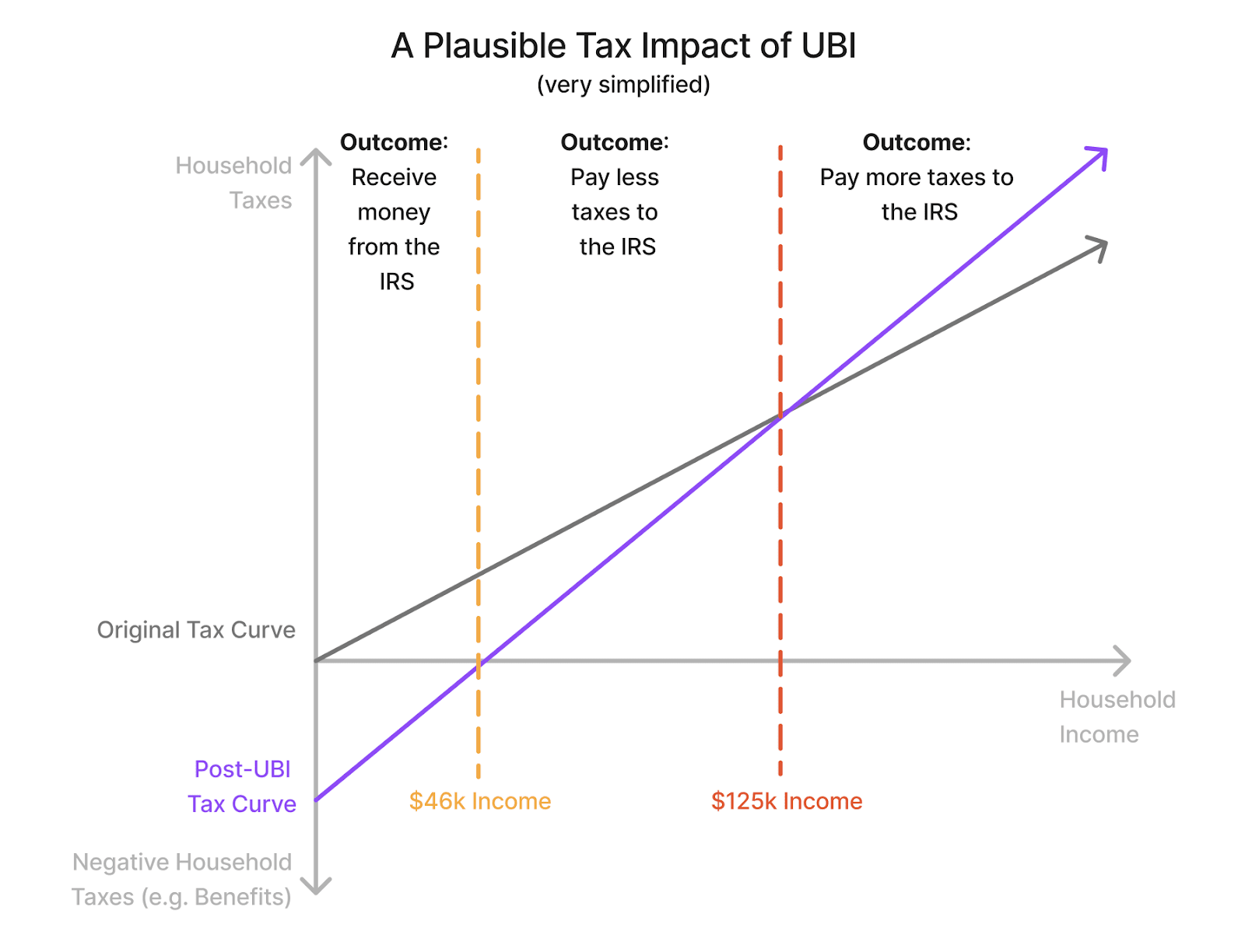

Let’s model what a practical implementation of UBI tax credits looks like today. For simplicity’s sake, let’s assume you’re in California, and individual income taxes are bumped up 30% across the board to pay for UBI. Here’s a rough approximation of how your taxes would change:

Below ~$46k[10]: you’d receive a recurring check from the IRS for $12,000 minus your personal taxes. At $46k, you’d pay roughly $0 net taxes.

From ~$46k to ~$125k[11]: you’d save somewhere between $0–$12,000 in taxes via a UBI tax credit. At $125k, you’d pay roughly the same as your net taxes today.

- From ~$125k upwards: you’d just pay more in total taxes after income tax reform and a UBI credit.

Does this sound less exciting than receiving money in the mail every month? I certainly thought so. In practice, for households making above ~$46k today, UBI would be just a (massively complicated) tax adjustment, not an actual supplemental income.

What is the actual goal of a UBI policy?

Let’s take a step back from this exercise. What’s our end goal here, and why are we even considering the gigantic challenge of fundamentally restructuring the US tax and budgetary system?

Presumably, we want UBI to protect against job automation. But really what we all mean when we say that is - we want a universal, simplified safety net that protects the disadvantaged, unemployed, and lowest-income individuals in our society.

Doing this analysis, it’s apparent to me that the means don’t justify the ends here. I don’t support UBI because I want to totally overhaul the US tax and budget system (though I do support higher taxes on the wealthy). I support UBI because I believe in a philosophy of basic human rights in a world soon-to-be-dominated by AI.

It seems, to me, that the main point of UBI is to protect the first category of people (earning under $46k a year) and provide them with a basic income so they can worry less about their basic needs.

Is there a more limited-scope policy that directly targets this category of people? There is! It’s called a negative income tax.

When you say you want UBI, why you actually just want a negative income tax

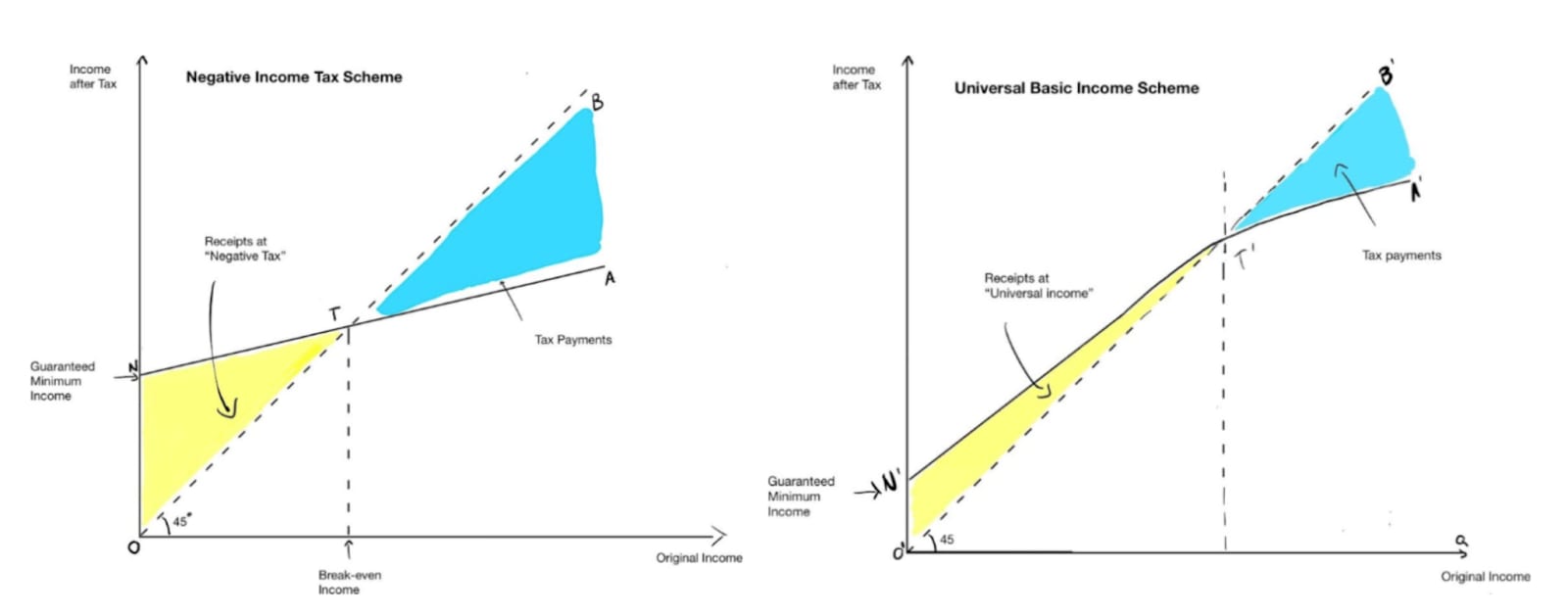

A negative income tax is exactly what it sounds like. Below a certain threshold, your income tax is negative, and the government will pay (subsidize) to you a recurring payment instead of you paying taxes. As your income increases, this benefit reduces. At some level of income (e.g. ~$46k), you’ll stop being paid by the government, and start paying taxes normally.

Does this sound somewhat familiar to the UBI system I described above? That’s because it is – a negative income tax (NIT) is nearly economically identical to a universal basic income. From an economic perspective, it is possible to set up a NIT and a UBI system such that the financial end result for individuals is the same.

This article from the Adam Smith Institute explains more thoroughly, and includes a helpful diagram showing the impact of an NIT and UBI on tax rates:

Of course, it must be noted that there are other very important differences between the two schemes such as payment frequency and timing[12], and the actual implementation (particularly marginal tax rates) matters a ton.

Why would you prefer a negative income tax (NIT) to UBI? I can identify a few main reasons:

- A NIT can be targeted in scope and cost: Instead of adjusting the tax treatment and benefits for the entire nation, you can solely focus on the category of individuals earning below ~$46k: the people most impacted by UBI anyways.

A rough estimate suggests you could drastically reduce the tax bill from the $3.96 trillion previously described to perhaps around $650 billion[13].

- Consequently, you could avoid the universal tax reform required to fund and account for UBI.

- It doesn’t require replacing the entire social welfare system: On top of such a reform being regressive as previously described, eliminating existing social programs would result in massive political blowback.

- It’s more politically feasible: For the reasons above, and because NIT can be viewed as a means-tested program with historical precedent rather than a universal entitlement.

Importantly, a negative income tax can still achieve the same goals as UBI: a comprehensive safety net for the disadvantaged.

The US already has a (limited) negative income tax in place!

A negative income tax is nothing new to the US government. Back in the 1960s, the Reagan administration proposed the Family Assistance Plan (basically a NIT for families) and conducted several studies, none of which were well-run enough to be conclusive.

However, the ideas from this era weren’t discarded. In 1975, Ford’s administration implemented the Earned Income Tax Credit (EITC), which has been continuously expanded numerous times in the past 50 years.

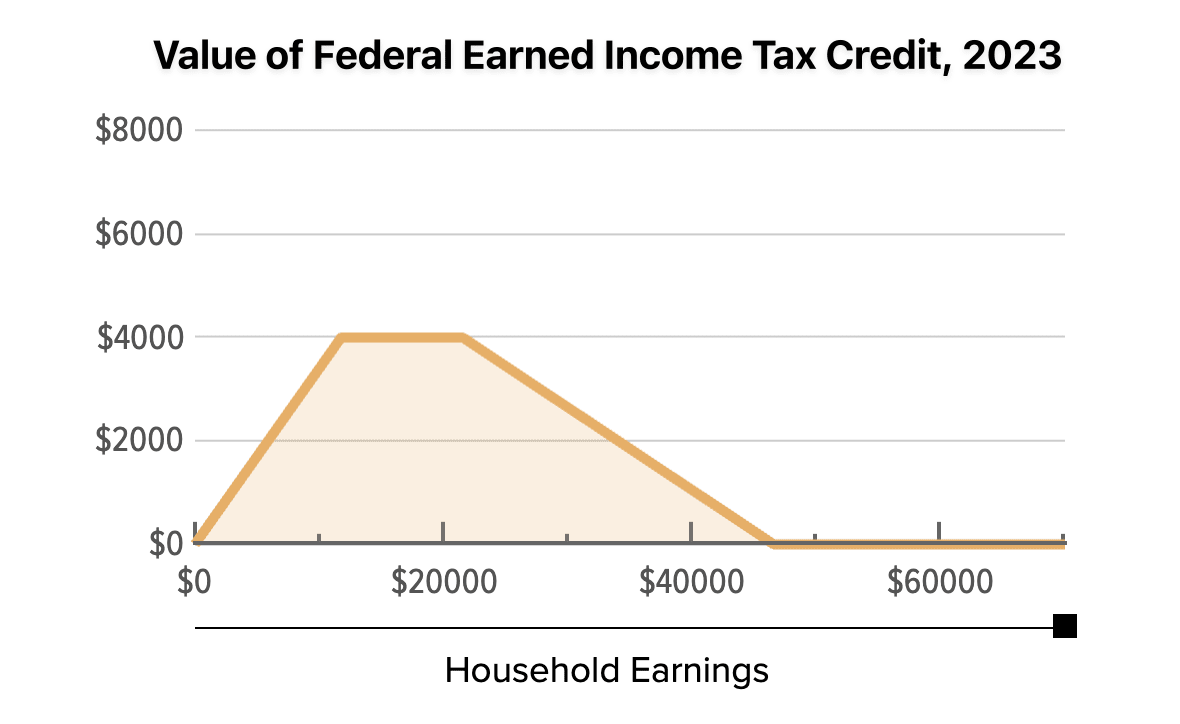

In essence, the EITC is a negative income tax for low to middle-income Americans that provides primarily tax credits, not direct payments. That is, it provides no additional income for the unemployed, but reduces taxes conditioned on participation in the labor force. You can see how it works in this diagram:

The EITC has been an extraordinarily effective and widely regarded tool for reducing poverty in the US. Recent data showing that it lifted about 5.6 million people, including 3 million children, above the poverty line in 2018, and studies have linked the EITC to improved school performance and higher college attendance rates.

It differs from a “pure” NIT (that includes direct payments) in only two respects:

- It’s heavily skewed towards individuals with dependents (e.g. children), with a maximum value of $600 in 2023 with no dependents but a maximum value of $7,430 for 3+ dependents.

- It doesn’t provide unconditional payments to the unemployed, instead providing maximal tax benefits for those earning between $10k and $25k.

This second point is the core ideological difference between the EITC and a “pure” NIT, and is likely the main reason a NIT doesn’t already exist in the US. Let’s quickly deep-dive into why this is the key problem.

UBI / NIT policies reject the premise that “free-riders” must be discouraged, in contrast to basically all US economic policy

It’s well known that here in the US, we’re allergic to any type of program that provides “handouts”. Similarly, we strongly prefer systems that encourage maximizing employment and minimize “free-riding”:

- We’re the only industrialized country that doesn’t provide universal healthcare.

- Our Social Security program is only available contingent on individuals contributing themselves for 10+ years.

- Federal welfare programs such as SNAP have work requirements to receive benefits.

- Our (relatively small) unemployment benefits are contingent on actively seeking employment (“3 work search activities per week”, as if the state government is your tiger mom giving you the keys to the Honda Civic).

As a result, the EITC avoids direct payments for the lowest-income Americans as a core feature, not a bug. It’s intended to provide financial support alongside a strong incentive to work, as opposed to UBI / NIT (which have heavily debated incentives to work, depending on who you ask).

Because of its requirement to earn income, the EITC has been heralded for generating “strong labor supply incentives”[14]. Multiple studies have shown that the EITC has created “increases in employment among low-skilled unmarried mothers”[15], attributing to it up to “one-third of single mothers’ employment growth throughout the 1990s”[16].

Do you think good economic policy should incentivize people like single mothers to work, or provide them with unconditional benefits? If you’re an advocate of UBI, you might support the latter. However, it’s very clear where the US currently stands on this question - it’s strongly against unconditional payments.

In short - if you want direct payments for all to be politically viable, first you need to shift the deeply American worldview that we should minimize handouts and encourage employment at all costs.

Relatively minor tweaks to the EITC would achieve most of the goals of UBI

Redesigning tax policy effectively is hard and probably outside the scope of this article. But even from this quick analysis, we can identify a simple set of changes to the EITC that would get us 90% there.

If you want to provide an income safety net for all Americans, you likely support the following changes:

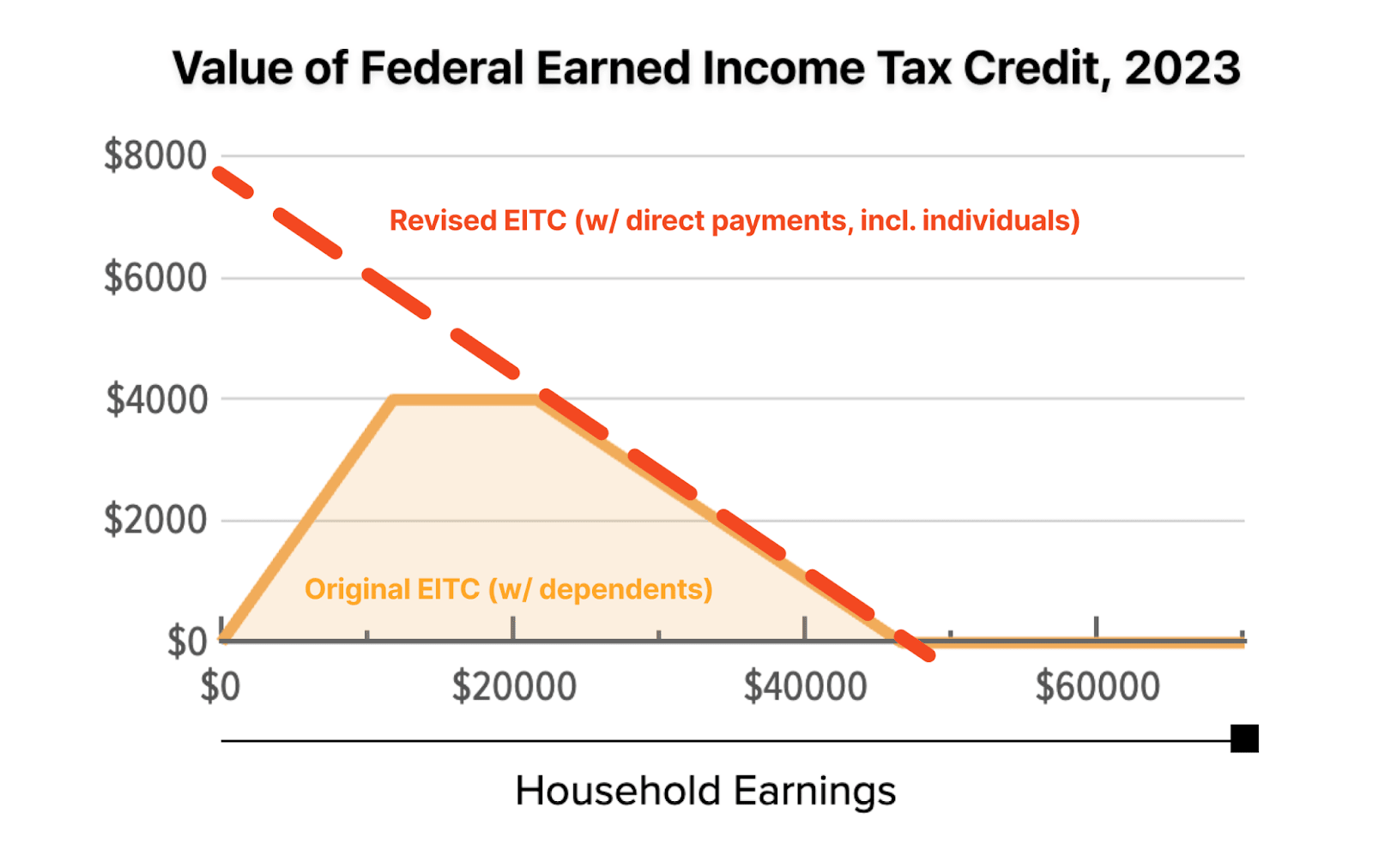

- Expand the EITC to provide a greater tax credit for individuals without dependents (currently max $600). That is, shift the EITC to also prioritize reducing poverty for individuals, not just families.

- Revise the EITC to provide direct payments to the unemployed, instead of cutting them out of the EITC to encourage greater employment.

These changes would establish a minimum basic income for all American citizens at roughly ⅙ of the cost of a generic UBI proposal today[17]. Here’s a simple diagram to visualize how this change would look:

Beyond this, you’d just need some tax finagling to provide these direct payments upfront and on a monthly basis, rather than as a lump sum in the following calendar year (after tax season).

Let’s summarize!

Here’s the high-level takeaways I learned from doing this research:

- Actually implementing the prototypical definition of UBI (e.g. $1k / citizen / month) leads to unnecessary taxation & budgetary chaos.

- Reforming income taxes would probably be necessary to “pay” for UBI.

- Tax credits would be handed out to everyone already paying over $12k in taxes. Middle to high-income individuals would see a mix of increased taxes and tax credits.

- On paper, the total budget increases by trillions of dollars, even though much of it is directly canceled out between higher taxes and immediate tax credits.

- Replacing existing social welfare programs with funding for UBI 1:1 is likely a regressive transfer that will result in value flowing from disadvantaged to the more-advantaged.

- Guaranteeing all citizens with a minimum baseline income is NOT the same as the prototypical definition of UBI. You can guarantee a minimum income without transferring payments to all citizens.

- A well-designed negative income tax (NIT) massively shrinks the scope & cost, and probably increases the political feasibility of UBI.

- The US already has a limited negative income tax - it’s called the Earned Income Tax Credit (EITC). The main differences from a “pure” NIT are:

- It strongly prioritizes families.

- It provides benefits only for the employed.

- As a nation, we haven’t already implemented a basic income in large part because of our cultural focus on maximizing employment and minimizing handouts.

- 2-3 key revisions to the EITC would be sufficient to match the high-level goals of UBI. You could achieve most of the same outcomes for about ⅙ the budget and tax impact.

Hope this was useful to read, and I’m happy to chat in the comments! There’s plenty I can still learn on these topics, and I don’t profess to be anything more than adequate in my knowledge of economic theory.

Some things I didn’t discuss:

- The important difference in timing of payments between UBI (monthly payments up front) and NIT (yearly payments after tax filing), and how it impacts the poor.

- Revising US unemployment benefits to achieve similar outcomes.

- Re-introducing the expanded Child Tax Credit, which essentially was a UBI-like policy for families with children for one year post-COVID.

- ^

Note: There are a variety of “guaranteed income” experiments today that target specific demographics of need, rather than all citizens. I’d argue that actually implementing them will look more like existing means-tested programs or the negative income tax described later in this article than the most popular concept for UBI.

- ^

Though the EU has been successful at forcing global companies to abide by its policies (such as in data privacy or port standardization). It’d certainly be possible for the EU to leverage its citizens to enforce some form of a wealth redistribution policy on American corporations.

- ^

Other methods include expected reductions in homelessness spending, incarceration, or higher expected tax revenues from increased consumer spending.

- ^

“The UBI is to be financed by getting rid of Social Security, Medicare, Medicaid, food stamps, Supplemental Security Income, housing subsidies, welfare for single women and every other kind of welfare and social-services program”. Charles Murray is a highly controversial and conservative economist. Read more.

- ^

- ^

Also, people (read: septuagenarians with political power) who have been paying into Social Security for decades are simply not going to accept slashing their benefits. At $1.3 trillion, this is the largest piece of the “social welfare” pie.

- ^

A common solution to this is to give social welfare recipients the choice between their existing programs or UBI. Of course, this modification means the main beneficiaries of UBI ends up being those not on social welfare.

- ^

Yes, modern monetary theory implies that we could just acquire more debt indefinitely or deal with rampant inflation. Because this is a massive and recurring financial bill, let’s assume that some type of budget balancing here is economically rational.

- ^

I’ll revisit this assumption in Part 2 evaluating corporate income taxes.

- ^

Talent.com estimates in April 2024 that with income of $46k in California, your current tax bill is $9.14k. If you pay 1.3x that, your tax bill is $11.88k.

- ^

Talent.com estimates in April 2024 that with income of $125k in California, your current tax bill is $40.66k. If you paid 1.3x that, you’d end up paying approximately $12.19k extra in tax.

- ^

UBI is typically paid in advance and monthly, while NIT is usually calculated and paid retrospectively based on the previous year's income.

- ^

Statista suggests 33% of US households earn under $50k a year. Assuming a uniform distribution of household income below this threshold (which is definitely incorrect) and linearly decreasing benefits from $12k at $0 income to $0 at $50k income, you could roughly estimate the total payments of such a NIT to be $12k * 330 million * .33 * 0.5 = $650 billion.

- ^

- ^

Ibid.

- ^

Ibid.

- ^

See “A NIT can be targeted in scope and cost” above for where these rough estimates come from.

SummaryBot @ 2024-05-14T13:05 (+1)

Executive summary: While universal basic income (UBI) is a popular idea to address job automation, a targeted negative income tax (NIT) or tweaks to the existing Earned Income Tax Credit (EITC) would be more practical and effective at providing a safety net.

Key points:

- Implementing a $12k/year UBI would be extremely expensive, requiring major tax increases and budget restructuring.

- Replacing existing welfare programs with UBI would be regressive, moving money from the disadvantaged to the more advantaged.

- For most people, UBI would function as a tax credit rather than additional income.

- A negative income tax (NIT) could provide a targeted safety net at a fraction of the cost of UBI.

- The US already has a limited NIT in the form of the EITC, which could be expanded to better match UBI goals by increasing benefits for individuals and providing payments to the unemployed.

- Cultural resistance to "handouts" and preference for encouraging employment are major obstacles to implementing UBI or NIT in the US.

This comment was auto-generated by the EA Forum Team. Feel free to point out issues with this summary by replying to the comment, and contact us if you have feedback.