Chip Production Policy Won’t Matter as Much as You'd Think

By Davidmanheim @ 2025-08-31T18:58 (+33)

tl;dr - If timelines are short, it’s too late, and if they are long (and if we don't all die,) the way to win the "AI race" is to generate more benefit from AI, not control of chip production.

Addendum: In the discussion in the comments, Peter makes good points, but I conclude: "this is very much unclear, and I'd love to see a lot more explicit reasoning about the models for impact, and how the policy angles relate to the timelines and the underlying risks."

Addendum 2.a: See conversation with @Erich_Grunewald 🔸 in the comments, where he made several important points that I think should materially change the conclusions - not enough to say that Chip Production policy will matter, but likely that chip export controls would.

Addendum 2.b: @Steven Byrnes has pointed out that the pressure differential from a Brita doesn't work the way I udnerstood. I have not figured out what is happening, and am far more comfortable with the economics than with the physics - so I think the analogy about counter-pressure works regardless of the dynamics for Brita filters.

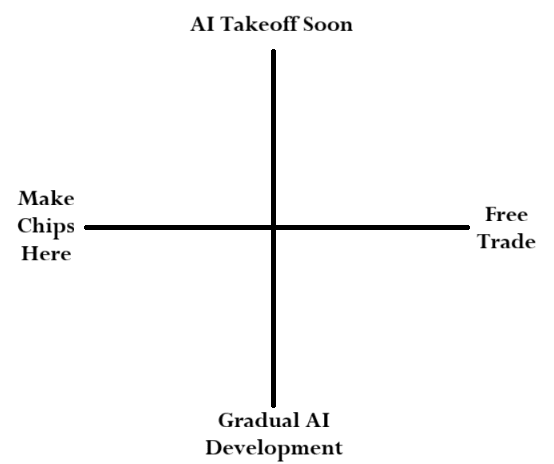

In AI policy, there’s a lot of focus on the speed frontier AI develops and becomes increasingly important for the economy, and creates substantial new risks of loss of control. There is also a lot of focus on the chips needed for training and running the frontier models, which involves industrial policy around who has the chips, and who can make them. This leads to a questionable narrative around the race for AGI, but even before we get to that question, there’s a simple question about the dynamics of the two dimensions.

If AI takeoff is fast, the question of where the chips will be located is already determined - policies for building fabs and energy production matters over the next decade, not before 2028. So if AI takeoff happens soon, and (neglected third dimension,) if control of the chips actually matters because the AI takeoff doesn’t kill us all, then running the race and prioritizing industrial policy over free trade doesn’t make sense, it’s too late to matter.

We’re living in a world where AI is going to have severe economic impacts, even if it doesn’t take off. And so for the rest of this discussion, let’s assume we’re in the lower half of the diagram.

And if the AI development is gradual - and by gradual, I mean the bearish predictions of an extra 1-5% annual GDP growth from AI by 2030, which could produce a durable economic advantage to the West over China, if it’s somehow kept here - then who makes the chips matters very little. We’ll see diffusion of the tech and deployment of the models everywhere long before differential GDP growth creates any kind of decisive advantage. In that world, we care a lot more about differential adoption of AI, not who owns the chips.

The stuff that creates growth, i.e. AI chips, which will increasingly be identical to what economic theory refers to as capital, will try hard to migrate to wherever it can do the most good economically. This is the free-market economic equivalent of gravitational attraction; it’s a fundamental force driven by human self-interest. Keeping it from happening in the short term might work, but it requires increasing effort and eventually indefinite amounts of effort to maintain in an open system.

And this is a fundamental issue with breaking markets. Policies can create incentives to change the relative price, but unless you stop all trade, markets will find increasingly desperate ways to equalize pressure. Tariffs can increase relative prices, but not stop movement of goods - unless they make it uneconomical to import the item.

Western countries could make all the chips, whether in Taiwan o in the US, but couldn’t fully keep chips from moving to where they are wanted any more than the US can keep everyone from buying Russian oil - they can only marginally change relative prices with increasingly severe sanctions and pressures. As economists often say, banning things is (usually) just imposing a large tax. And that means we can have a limited impact on where chips go. (Even location verification is inevitably going to be only partially effective, albeit effective at further marginally changing the costs.) So this prediction is just making the kind of obvious point that we’ll see smuggling as long as it’s insanely profitable to do it.

If you’ve ever overfilled a Brita pitcher, you’ll recognize the equivalent scenario - the filter creates pressure, but unless you can stop the flow completely, you’re just talking about slight changes to the relative level in the top and bottom section. Removing the filter would equalize pressure, but unless you can stop all flow between sections, you can’t keep all the water in the top section.

So where will the chips go? Wherever it’s most lucrative to put them, modulus costs.

Of course, increasing clean power production, baseload and storage, and getting prices much lower, is stupidly good policy regardless of AI. And for determining how lucrative data centers are, it is going to matter at least as much as where chips are made, and moved to. So even if we somehow cut off the best chips completely, and China infeasibly stays a generation behind the West on their chip production in the intermediate term, chips that are 25% as efficient are still better for at least inference as long as energy prices are less than 25% of what they are in the West. So in equilibrium they end up with more of the data centers unless the west keeps the difference in power prices and price differences from export controls.

So yes, data centers will migrate to where the overall costs of chips + power are cheap - but this isn’t the end of the story, because location of the data center really only matters for HFT. And in worlds where China has 100% of the chip production, and power that’s half as expensive, if OpenAI is willing to pay twice what Chinese companies will for the resulting compute, there will be lots of pressure to locate the datacenters in places where OpenAI is willing to pay for it. (Which probably isn’t inside of China, given the infosec risks.)

What matters in a (relatively near-term) equilibrium is who can get the most use out of the models, and I think policy discussion are mostly ignoring this point. If total compute remains limited, the highest-value applications will pay enough to saturate their needs, just like OpenAI and other Western firms are saturating NVIDIA’s production capacity today. If Chinese companies are allowed to automate their factories with GPT 6 agents and US companies cannot, they’ll pay to use the models, and reap the benefits of economic growth. And if Americans can’t pay for GPT-6 psychologists, they won’t pay to use the models, and won’t get the benefits of reduced mental healthcare costs - which seem kind of important as the world accelerates and joblessness for young males increases (with all the likely tragic implications.)

So for all the handwringing, in worlds where economic power drives differential advantage, the chip production location has limited impact - not none, but nothing like the decisive advantage that seems to be implied. Power production has additional but still limited impact. The end beneficiaries of the growth will be whoever uses the AI, albeit as slightly modified by the price differentials created by these policies. And that means the real race is about deregulation and economic growth uber alles - which the AI industry in the US has recently realized.

So in summary, the idea that the US will create a sustainable advantage from magically moving industrial production to the US (which itself is… hard) and then actually permitting power (which we seem not to be doing,) is mostly a fantasy. But this runs both ways; if the chips help US companies more than they help countries elsewhere, the growth created by the chips will be inevitably accrue here, and vice-versa. (And cutting off trade, much less internet access, so that you can keep the chips from being used for growth elsewhere is defeating the point - you’re destroying the thing needed for growth.)

Of course, this leads to increasingly dangerous attempts to race towards unrestricted capabilities imposing uninternalized externalities on the public - there needs to be some regulation. But it seems to me that chip restrictions, and all the attendant industrial policy promoting race dynamics are not the way.

Thanks to Sean O hEigeartaigh and Mathieu Putz for comments on an earlier version of this post.

Peter Wildeford @ 2025-08-31T21:37 (+41)

Hi David - I work a lot on semiconductor/chip export policy, so very important to think about the strategy here.

My biggest issue is that "short vs. long" timelines is not a binary. I agree that under longer timelines, say post-2035, China likely can significantly catch up on chip manufacturing. (Seems much less likely pre-2035.) But I think the controls logic matters really strongly for timelines 2025-2035 and still might create a larger strategic advantage post-2035.

Who has the chips still matters, since it determines whether the country has enough compute to train their own models, run any models, and provision cloud providers. You treat "differential adoption" and "who owns chips" as separate when they're deeply interconnected. If you control chip supply, you inherently influence adoption patterns. There would be diffusion of AI of course, but it would be much more likely to come from the US given chip controls, and potentially the AI would remain on US cloud under US control.

Furthermore, if you grant that AI can accelerate AI development itself, a 2-3 year compute advantage could be decisive... and not just in "fast take-off recursive self-improvement" but even in mundane ways where better AI leads to better chip design tools, better compiler optimization better datacenter cooling systems, and better materials science for next-gen chips.

You're right that it is impossible to control 100% of the chips, but that's not the goal. The goal is to control enough of the chips enough of the time to create a structural advantage. Maintaining a 10-to-1 compute advantage of the US over China will mean that even if we had AI parity, we'd still have 10x more AI agents than China. And we'd likely have better AI per agent as well.

For example, consider the same Russian oil example you discuss - yes, there's significant leakage to India and China and these controls aren't perfect, but Russia's realized prices have stayed ~$15-20/barrel below Brent throughout 2024-2025 - forcing Russia to accept steep discounts while burning cash on shadow fleet operations and longer shipping routes.

And chips are much easier to control than oil right now. Currently, OpenAI can buy one million NVIDIA GB300s to power Stargate, but China and Russia can't even come close. Chinese chips are currently much weaker in both quantity and quality, and this will persist for awhile as China lacks the relevant chipmaking equipment and likely will for some time -- the EUV tech that prints chips at nanometer scale took decades to develop and is arguably the most advanced technology ever made. You seem to have some all-or-nothing thinking here or think that we can't possibly block enough chips to matter, but we already have significantly reduced China's compute stock and you even have people like DeepSeek's CEO mentioning that chip controls are their biggest barrier. Chinese AI development would certainly be different if China could freely buy one million GB300s as well.

The key thing is that semiconductor manufacturing isn't a commodity market with fungible goods flowing to equilibrium. You're treating this as a standard economic problem where market forces inevitably equalize and assume a lot of frictionless markets - but neither of these seem true. The chip supply chain has unique characteristics with extreme manufacturing concentration, decades-long development cycles, and tacit knowledge that make it different. Additionally, network effects in AI development could create lock-in before economic pressure equalizes access. Moreover, American/Western AI and chip development isn't going to freely flow to China because the US government would continue to stop that from happening as a matter of national security. Capital does flow, but this technology cannot flow quickly, freely, or easily.

It's also not easy to just arbitrarily make up for chip disadvantage with energy advantage. It's very difficult to train frontier AI models on ancient hardware. DeepSeek has been trying hard all year to train their model on Huawei chips and still haven't succeeded. It doesn't matter how cheap you make energy if chips remain a limiting factor. Arguably, TSMC's lead over SMIC has grown, not shrunk, over the past decade despite massive Chinese investment.

All told, I think that China is at a significant AI disadvantage over the next decade or more and this is due to reasonably effective (albeit imperfect) chip controls. Ideally we would make the chip controls even better and stronger to press that advantage further (I have ideas on how), but that's a different conversation from the strategic wisdom of the controls in the first place.

Davidmanheim @ 2025-09-01T06:19 (+8)

First, I was convinced, separately, that chip production location matters more than I presumed here because chips are not commodities in an important way I neglected - the security of a chip isn't really verifiable post-hoc, and worse, the differential insecurity of chips to US versus Chinese backdoors means that companies based in different locations will have different preferences for which risks to tolerate. (On the other hand, I think you're wrong in saying that "the chip supply chain has unique characteristics [compared to oil,] with extreme manufacturing concentration, decades-long development cycles, and tacit knowledge that make it different" - because the same is true for crude oil extraction! What matters is who refines it, and who buys it, and what it's used for.)

Second, I agree that the dichotomy of short versus long timelines unfairly simplifies the question - I had intended to indicate that this was a spectrum in the diagram, but on rereading, didn't actually say this. So I'll clarify a few points. First, as others have noted, the relevant timeline is from now to takeoff, not from now to actual endgame. Second, if we're talking about takeoff after 2035, the investments in China are going to swamp western production. (This is the command economy advantage - though I could imagine it's vulnerable to the typical failure modes where they overinvest in the wrong thing, and can't change course quickly.)

On the other hand, for the highest acceleration short timelines, for fabrication, we're past the point of any decisive decisions on chip production, and arguably past the point of doing anything on the hardware usage to decide what occurs - the only route to control the tech is short term policy, where only the relative leads of the specific frontier companies matters, and controlling the chips is about maintaining a very short term lead that doesn't depend on technical expertise, just on hardware. (I'm skeptical of this - not because it's implausible, but because the cost of these fights is high. That is, I think it's more likely that in these worlds the critical risk mitigation is global cooperation to stop loss of control - which means that the fights being created over hardware are on net damaging!)

For moderately short, 2-6 year timelines, the timelines for chip fabs are long enough that we're mostly locked in not just to overall western dominance via chips produced in Taiwan, but because fabrication plans built today are coming online closer to 2029, and the rush to build Chinese fabrication plants is already baked in. And that's just the fabs - for the top chips, the actual chip design usually takes as long or longer than building the plant. So we're going to see shifts towards the end of the window either way.

And in those moderate timeline worlds, I'll strongly grant your point that location, in terms of which companies have the technical lead for producing AGI, matters at lot. I just don't see it as impacted that much by chip embargoes, which will be circumvented either by smuggling, or by leasing the chips via proxies, etc. And as with the above scenario, I think that hobbling Chinese acquisition of chips turns this into a zero-sum game along the wrong dimension - because the actual force dictating which AI companies have access to the most compute is the capital markets, and expectations for profit. But this brings in a point I didn't discuss at all here, and wasn't thinking about, where AI companies have commodified their own offerings. Capital market expectations seem not to be accounting for this - or are properly pricing both the upside of a single-company AI singleton, and the downside of commodified offerings meaning there's no profit at all.

Either way, I'm unsure that western countries should see much marginal benefit in the coming years from controlling chip location. "Hobbling" Chinese AI efforts is still easier to do via current market dynamics where western companies have better market options, and will pay more for the chips - if that's even a benefit, which seems very unclear given the commodification of models and the benefit accruing to the users of AI models.

So my conclusion is that this is very much unclear, and I'd love to see a lot more explicit reasoning about the models for impact, and how the policy angles relate to the timelines and the underlying risks - which are very much missing in the public discussions I've seen.

Erich_Grunewald 🔸 @ 2025-09-01T14:24 (+9)

On the other hand, I think you're wrong in saying that "the chip supply chain has unique characteristics [compared to oil,] with extreme manufacturing concentration, decades-long development cycles, and tacit knowledge that make it different" - because the same is true for crude oil extraction! What matters is who refines it, and who buys it, and what it's used for.

I think the technical barriers to developing EUV photolithography from scratch are far higher than anything needed to extract, refine, or transport oil. I also think the market concentration is far higher in the AI chip design and semiconductor industries. There's no oil equivalent to TSMC's ~90% leading-edge logic chip, NVIDIA's ~90% data center GPU, or ASML's 100% EUVL machine market shares.

Second, if we're talking about takeoff after 2035, the investments in China are going to swamp western production. (This is the command economy advantage - though I could imagine it's vulnerable to the typical failure modes where they overinvest in the wrong thing, and can't change course quickly.)

Are you sure? I would guess that the chip supply chain used by NVIDIA has more investment than the Chinese counterpart. For example, according to a SEMI report, China will spend $38bn on semiconductor manufacturing equipment in 2025, whereas the US + Taiwan + South Korea + Japan is set to spend a combined ~$70bn. I would guess it looks directionally similar for R&D investment, though the difference may be smaller there.

For moderately short, 2-6 year timelines, the timelines for chip fabs are long enough that we're mostly locked in not just to overall western dominance via chips produced in Taiwan, but because fabrication plans built today are coming online closer to 2029, and the rush to build Chinese fabrication plants is already baked in. And that's just the fabs - for the top chips, the actual chip design usually takes as long or longer than building the plant.

I was under the impression the AI chip design process is more like 1.5-2 years, and a fab is built in 2-3 years in Taiwan or 4 years for the Arizona fab. It sounds like you think differently? Whatever it is, I would guess it's roughly similar across the industry, including in China. That seems like, if my numbers are right, it leaves enough room for policy now to influence the relative compute distribution of nations 5-6 years from now.

Davidmanheim @ 2025-09-02T07:58 (+6)

Edit to add: First, I really liked your post yesterday, which responded to some of this.

I think the technical barriers to developing EUV photolithography from scratch are far higher than anything needed to extract, refine, or transport oil.

I think the technical barriers are higher today, but not so high that intense Chinese investment can't dent it over the course of a decade. SMEE is investing in laser-induced discharge plasma tech, with rumored trial production as soon as the end of this year. SMIC is using DUV more efficiently for (lower-yield, but still effective) chip production. There's also work on Nanoimprint lithography, immersion lithography, packaging, etc. And that won't affect market shares, until it does.

There's no oil equivalent to TSMC's ~90% leading-edge logic chip, NVIDIA's ~90% data center GPU, or ASML's 100% EUVL machine market shares.

I think Standard Oil in the late 1800s, and the seven sisters in the 1950s, both did something roughly similar - but this isn't actually key to the argument. (And as you pointed out in your piece, oil could be controlled - but that was because the seven sisters predated WWII, and were all on the Allied side. The same isn't true if China has started competing already - and they are trying to do so.)

But the key point I wanted to make is that oil only mattered because it enabled economic development. The long-term winners were definitely not the groups that extracted or refined the oil, even though they made lots of money - it was the countries that consumed the oil and built industrial capacity leading up to WWII, and could then use the controlled supply of oil.

And as far as I can tell, no-one is restricting Chinese companies from using compute right now - they don't own it, but can use the same LLMs I do. (But I guess it matter smuch more if we're primarily concerned with internal deployment?)

I would guess that the chip supply chain used by NVIDIA has more investment than the Chinese counterpart.

Sure, today, if you count all of the West versus China alone. But my point is that this will change over a decade or more - the Chinese government is happy to subsidize things if they look like they will work, and will be under increasing pressure to do so if there is a continuing embargo. If timelines are long, they have lots of reason to invest, and they have much longer investment timelines than western companies can typically manage. (Though the internal management of NVIDIA and similar have shown that they can plan for longer timelines then most investors will care about, as I'll note next.)

I was under the impression the AI chip design process is more like 1.5-2 years, and a fab is built in 2-3 years in Taiwan or 4 years for the Arizona fab.

TSMC Arizona was announced in May 2020, which makes it 5 years to first chip production. I think this is the most relevant timeline; Taiwan can keep building new fabs, and it keeps things locked in to the status quo, and China can't start building fabs using UV lithography tech they are still developing, so the lock-in is until closer to the end of the decade. (The second fab is planned to come online in 2028, and it will be longer for others - and the first fab is using their older 4nm process, while they have been using the 3nm process since 2022 in Taiwan, which will only start in the US in 2028 earliest, and they have started using the 2nm process this year, which will be in the 2028 second fab, or perhaps only in the planned-for-2030 third Arizona fab.)

And the "chip design process" is 2 years or so only after the specifications and design are basically finished - but my understanding is that those depend on having a roadmap that is far longer. For example, the public roadmaps for tech development from NVIDIA extend to the Feynman architecture planned for late 2028, based on using fabs that are coming online today, integrating Vera chips they are already making. (And which I'll guess won't be made in the 2nm plants they will have online in the US then.) That means they are confident enough in the roadmap to be pretty far along with high-level design already, but they still need 3+ years to get it into production. My understanding (which could be entirely wrong) was that the internal roadmap extends out a few more generations, and they have been investing in planning and tech development to enable their later chips even longer.

Erich_Grunewald 🔸 @ 2025-09-07T19:19 (+6)

On timelines, I think it's worth separating out export controls on different items:

- Controls on AI chips themselves start having effects on AI systems within a year or so probably (say 6-12 months to procure and install the chips, and 6-18 months to develop/train/post-train a model with them), or even sooner for deployment/inference, i.e. 1-2 years or so.

- Controls on semiconductor manufacturing equipment (SME) take longer to have an impact as you say, but I think not that long. SMIC (and therefore future Ascend GPUs) is clearly limited by the 2019 ban on EUV photolithography, and I would say this was apparent as early as 2023. So I think SME controls instituted now would start having an effect on chip production in the late 2020s already, and on AI systems 1-2 years after that.

Most other relevant products (e.g., HBM and EDA software) probably fall between those two in terms of how quickly controls affect downstream AI systems.

So that means policy changes in 2025 could start affecting Chinese AI models in 2027 (for chips) and around 2030 (for SME) already, which seems relevant to even short-timeline worlds. For example, Daniel Kokotajlo's median for superhuman coders is now 2029, and IIUC Eli Lifland's median is in the (early?) 2030s.

But I would go further to say that export controls now can substantially affect compute access well into the 2030s or even the 2040s. You write that

the technical barriers [to Chinese indigenization of leading-edge chip fabrication] are higher today, but not so high that intense Chinese investment can't dent it over the course of a decade. SMEE is investing in laser-induced discharge plasma tech, with rumored trial production as soon as the end of this year. SMIC is using DUV more efficiently for (lower-yield, but still effective) chip production. There's also work on Nanoimprint lithography, immersion lithography, packaging, etc. And that won't affect market shares, until it does.

I won't have time to go into great detail here, but I have researched this a fair amount and I think you are too bullish on Chinese leading-edge chip fabrication. To be clear, China can and will certainly produce AI chips, and these are decent AI chips. But they will likely produce those chips less cost-efficiently and at lower volumes due to having worse equipment, and they will have worse performance than TSMC-fabbed chips due to using older-generation processes. The lack of EUV machines, which will likely last at least another five years and plausibly well into the 2030s, alone is a very significant constraint.

On SMEE and SMIC in particular -- you write:

SMEE is investing in laser-induced discharge plasma tech, with rumored trial production as soon as the end of this year.

SMEE was established 23 years ago to produce indigenous lithography, and 23 years later it still has essentially no market share, and it still has not produced an immersion DUV machine, let alone an EUV machine, which is far more difficult. I would not be surprised if, when the indigenous Chinese immersion DUV machine does finally arrive, it is a SiCarrier (or subsidiary) product and not an SMEE product.

SMIC is using DUV more efficiently for (lower-yield, but still effective) chip production.

In what sense do you mean SMIC is using DUV more efficiently? It is using immersion DUV multi-patterning (with ASML machines) to compensate for its lack of EUV machines. But as you note this means worse yield and lower throughput. I don't see any sense in which SMIC is using DUV more efficiently; it's just using it more, in order to get around a constraint that TSMC doesn't have. In any case, multi-patterning with immersion DUV can only take you so far; there's likely a hard stop around what's vaguely called 2 nm or 1.4 nm process nodes, even if you do multi-patterning perfectly. (For reference, TSMC is starting mass production on its "2 nm" process this year.)

Davidmanheim @ 2025-09-09T12:03 (+2)

Thanks for this response - I am not an expert on chip production, and your response on fabrication is clearly better informed than mine.

However, "Policy changes in 2025 could start affecting Chinese AI models in 2027 (for chips) and around 2030 (for SME) already."

I now agree with this - and I was told in other comments that I didn't sufficiently distinguish between these two, so thanks for clarifying that. But 2030 for starting to help get more chips is long timelines, and the people you cite with 2029-2030 timelines expect it to be playing out already then, so starting to get more chips then seems irrelevant in those worlds.

Erich_Grunewald 🔸 @ 2025-09-07T18:36 (+6)

On the oil analogy, it seems from

The long-term winners were definitely not the groups that extracted or refined the oil, even though they made lots of money - it was the countries that consumed the oil and built industrial capacity leading up to WWII, and could then use the controlled supply of oil. ... And as far as I can tell, no-one is restricting Chinese companies from using compute right now - they don't own it, but can use the same LLMs I do.

that you think ownership of compute does not substantially influence who will have or control the most powerful AI systems? I disagree; I think it will impact both AI developers and also companies relying on access to AI models. First, AI developers -- export controls put the Chinese AI industry as a whole at a compute disadvantage, which we see in the fact that they train less compute-intensive models, for a few reasons:

- It is generally unappealing for major AI developers to merely rent GPUs they don't own, as a result of which they often build their own data centers (xAI, Google) or rely on partnerships for exclusive access (OpenAI, Anthropic). I think the main reasons for this are cost, (un)certainty, and greater control over the cluster set-up.

- Chinese companies cannot build their own data centers with export-controlled chips without smuggling, and cannot embark on these partnerships with American hyperscalers. If they want to use cutting-edge GPUs, they must either rely on smuggling (which means higher prices and smaller quantities), or renting from foreign cloud providers.

- The US likely could, if and when it wanted to, deny access of compute via the cloud to Chinese customers, at least large-scale use and at least for the large hyperscalers. So for Chinese AI developers to rely on foreign cloud compute gives the US a lot of leverage. (There are some questions around how feasible it is to circumvent KYC checks, and especially whether the US can effectively ensure these checks are done well in third countries, but I think the US could deny China most of the world's rentable cloud compute in this way.)

- Chinese privacy law makes it harder for Chinese AI developers to use foreign cloud compute, at least for some use cases. I'm not sure exactly how strong this effect is, but it seems non-negligible.

- For deployment/inference, you may want to have your compute located close to your users, as that reduces latency.

- In the event of an actual conflict over or involving AI, you can seize compute located on territory you control. I hope that doesn't happen obviously, but it's definitely a reason why as an AI developer you'd prefer to use compute located in your own country, than located in a rival country or one of the rival's allies or partners.

That's AI developers. As for the AI industry more broadly, there are barriers for Chinese companies wanting to use US models like ChatGPT or Claude, which, for example, is likely one reason why Manus moved to Singapore. So the current disparity in who owns compute and where it is located means Chinese AI developers are relatively compute-poor, and since Chinese companies rely substantially on domestic Chinese models, it seems to me like the entire Chinese AI industry is impacted by these restrictions.

Also, I disagree that oil "only mattered because it enabled economic development". In WWII especially, oil was necessary for fuel-hungry militaries to function. I think AI will also be militarily important even ignoring its effects on economic development, though maybe less so than oil.

Davidmanheim @ 2025-09-09T12:16 (+2)

I've updated substantially towards this view - the practical issues with renting CPUs make them far less of a fungible commodity than I was assuming, and as you pointed out, contra my understanding, there are effective restrictions on Chinese companies getting their hands on large amounts of compute.